Kospi surged 3.7% overnight on SK Hynix ADR demand ahead of Friday’s $29B Nasdaq debut. PepsiCo Q2 lands BMO. Fed minutes hawkish, oil above $78, Dow -1.1%.

TLDR

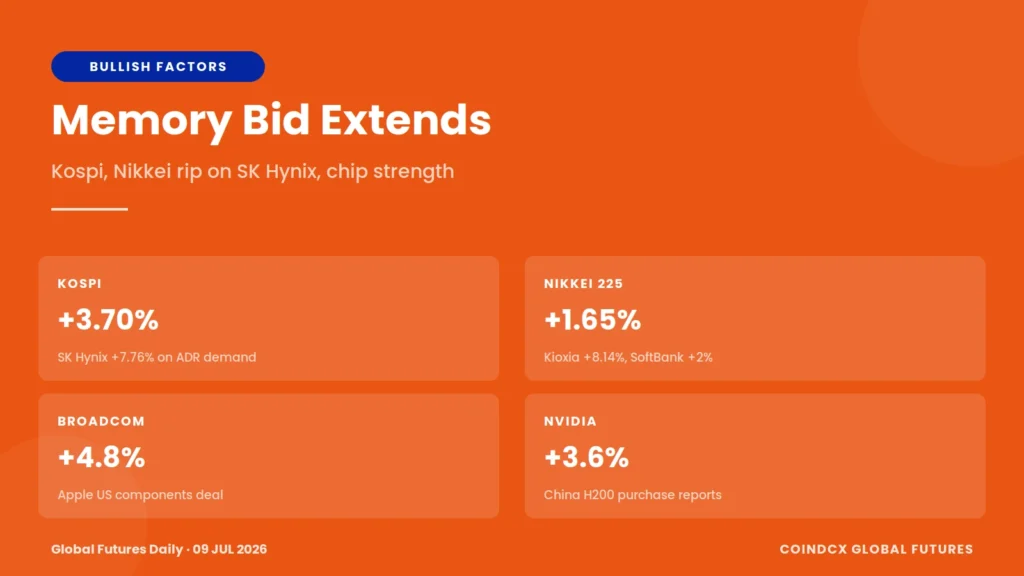

- Kospi ripped 3.7% overnight to 7,514.67 with SK Hynix +7.76% after its US ADR bookbuild was oversubscribed more than 7x ahead of Friday’s Nasdaq debut.

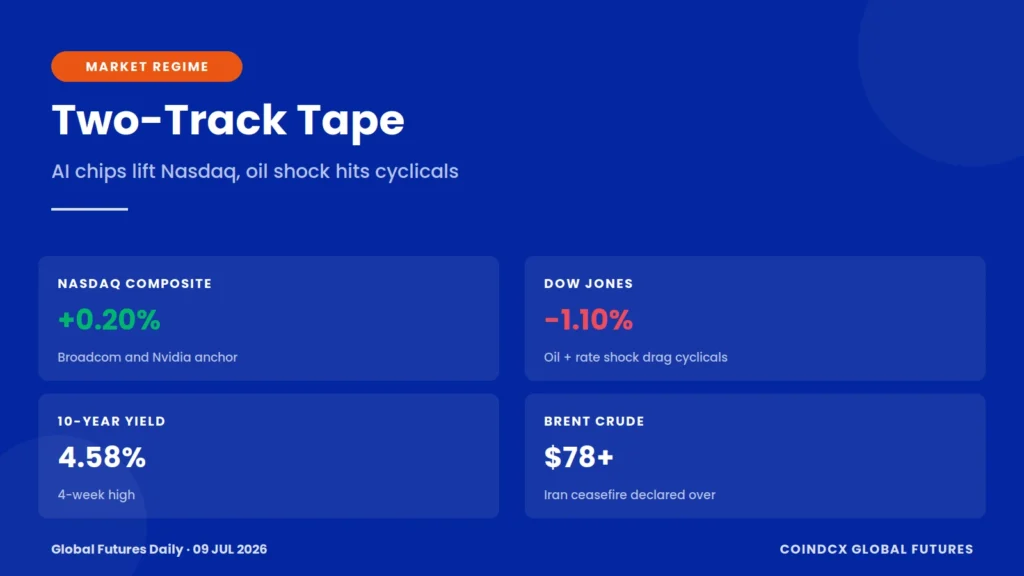

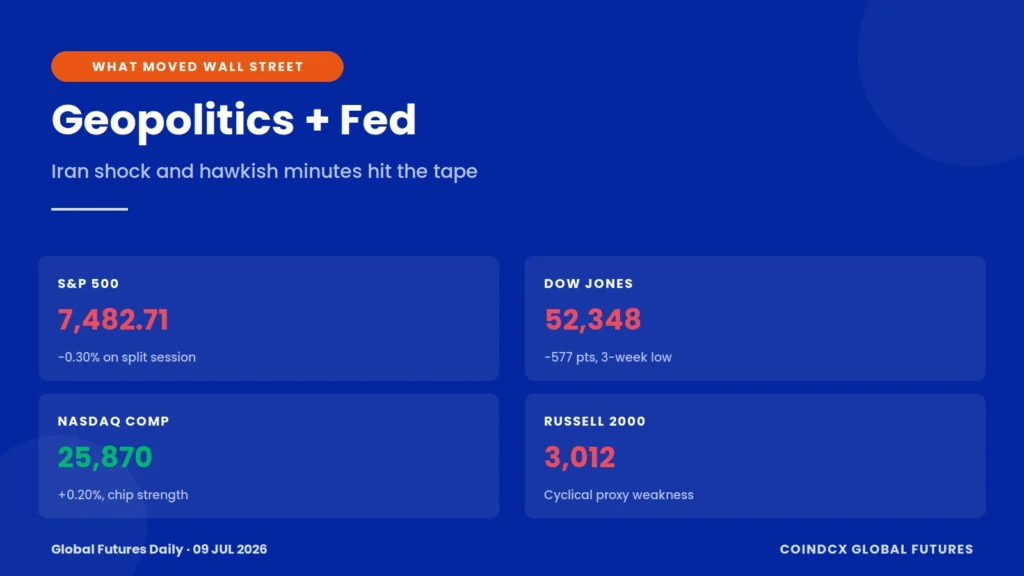

- Wall Street closed split on Wednesday. The Dow fell 1.1% to 52,348.39 on the Iran ceasefire escalation and an oil spike, while the Nasdaq Composite added 0.2% to 25,870.65 as Broadcom and Nvidia carried chip strength.

- June FOMC minutes revealed a divided committee, with a few officials making the case for a rate hike. The 10-year Treasury yield sits at 4.58%, a 4-week high.

- PepsiCo reports Q2 before the opening bell today. Street consensus is $2.21 EPS on $23.95B revenue, with estimates trimmed 1.3% over the past 30 days.

- Brent crude trades above $78 per barrel and WTI above $72 after a near 7% intraday spike Wednesday, adding a fresh inflation impulse into the July 14 CPI print.

Market Regime

The tape has entered a two-track regime where AI memory and chip strength keep the Nasdaq bid while cyclical, rate-sensitive, and energy-consuming sectors take the hit from a fresh oil shock. Wednesday’s split, Dow down 1.1% and Nasdaq up 0.2%, captured that dispersion cleanly. The 10-year yield holding 4.58% and June FOMC minutes exposing a Fed committee divided on the direction of policy have layered a second axis of rotation on top of the geopolitical one.

What could break the setup is any escalation on the Iran front that pushes Brent past $80 for a sustained stretch, or a hot PepsiCo print that pivots the consumer read into a cost-pass-through narrative right before next week’s CPI. What could extend it is a clean SK Hynix debut on Friday that confirms institutional demand for HBM exposure and revives the memory-led leadership pattern that has carried the Nasdaq higher through most of Q2.

Bullish Factors

- Kospi surged 3.7% overnight to 7,514.67, led by SK Hynix +7.76%, Samsung Electronics +4%, and broad memory strength.

- SK Hynix Nasdaq ADR listing lands Friday under ticker SKHY with a $29 billion raise, the largest foreign ADR offering in Wall Street history.

- Broadcom rose 4.8% Wednesday after expanding its US-made components deal with Apple, extending the AI supply-chain leadership pattern.

- Nvidia added 3.6% Wednesday on reports that Chinese firms plan to increase H200 chip purchases.

- US index futures traded modestly higher pre-open. Nasdaq 100 futures were up 0.43% and S&P 500 futures up 0.29% as risk sentiment recovered from the geopolitical shock.

- Nikkei 225 climbed 1.65% to 67,923.20 with Kioxia +8.14% and SoftBank +2%, extending the AI memory bid across the region.

- Shanghai Composite added 1.66% to 4,037 after the People’s Bank of China signaled it would keep monetary policy appropriately loose.

Bearish Factors

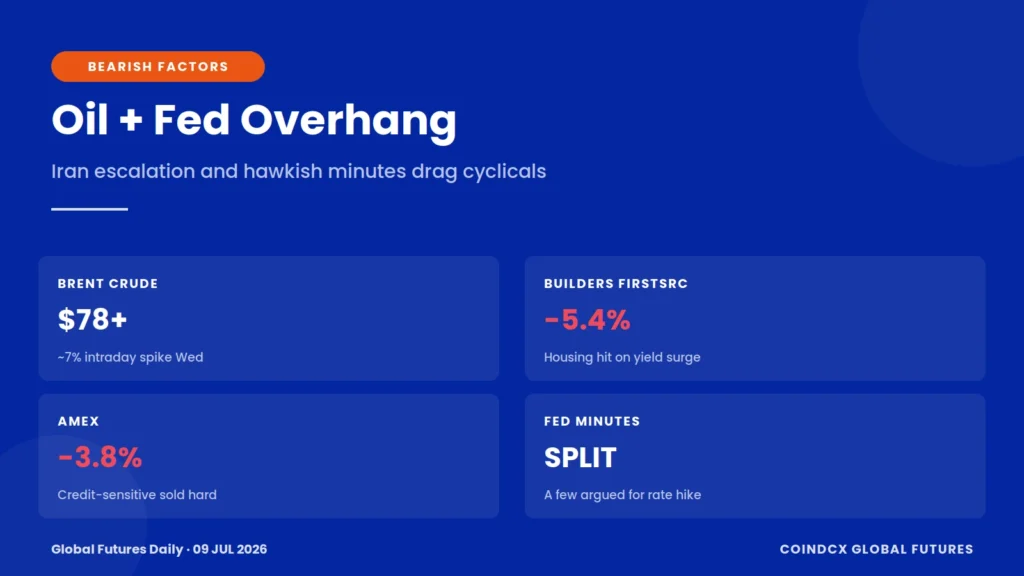

- President Trump declared the US-Iran ceasefire is officially over following renewed strikes on both sides, reintroducing a geopolitical risk premium into oil.

- Brent crude trades above $78 per barrel and WTI above $72 after a near 7% intraday spike Wednesday, feeding directly into inflation expectations.

- June FOMC minutes revealed a deeply divided committee. Several participants said they no longer view current policy as restrictive, and a few actively made the case for raising rates at the June meeting.

- The 10-year Treasury yield sits at 4.58%, a 4-week high, keeping mortgages, autos, and corporate borrowing expensive.

- Housing sold off hard on Wednesday. Builders FirstSource fell 5.4%, PulteGroup fell 5.4%, and D.R. Horton lost 4.6% as rate-sensitivity re-emerged.

- Cyclical Dow components were dragged lower. American Express fell 3.8%, Sherwin-Williams lost 3.5%, and Boeing fell 3%.

- PepsiCo consensus EPS has drifted down 1.3% over the past 30 days, signaling some caution on the consumer print heading into today’s report.

Asian Markets This Morning

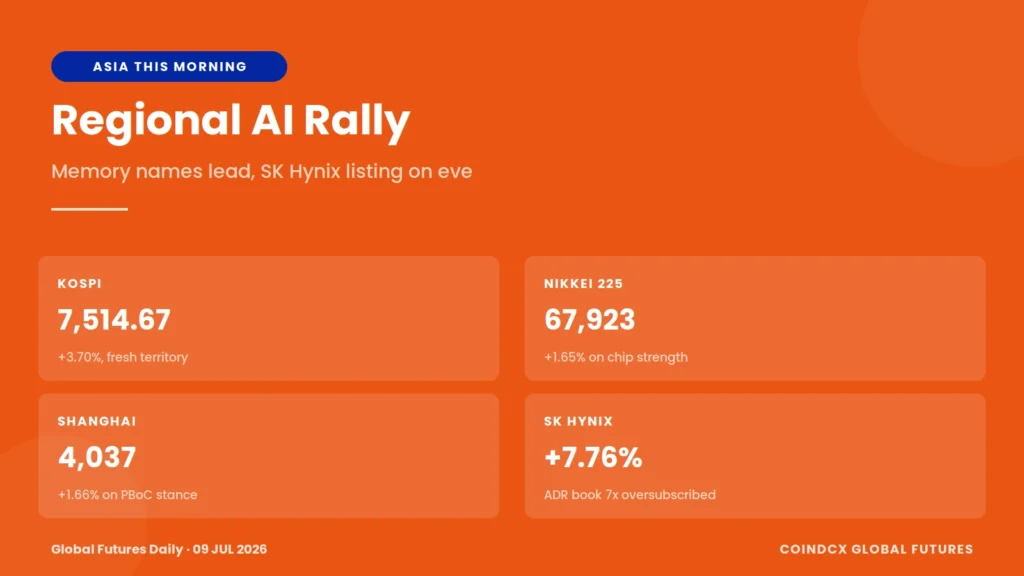

The Kospi led the region overnight with a 3.7% surge to 7,514.67, powered almost entirely by SK Hynix, which climbed 7.76% after its US ADR bookbuild was oversubscribed more than 7x. The Nasdaq listing lands Friday under ticker SKHY at an indicative price of $165.26 per receipt, raising approximately $29 billion, the largest foreign ADR offering ever recorded on Wall Street, surpassing Alibaba in 2014 and Saudi Aramco in 2019. Samsung Electronics added 4% on the memory follow-through.

The Nikkei 225 climbed 1.65% to 67,923.20 with Kioxia jumping 8.14% and SoftBank adding 2%. The Shanghai Composite added 1.66% to 4,037 after the People’s Bank of China signaled it would keep monetary policy appropriately loose and step up support for domestic consumption. The regional tape is running a clean HBM-and-AI leadership pattern that has decoupled cleanly from the Middle East oil narrative dominating Wall Street. Whether that decoupling holds into the SK Hynix debut tomorrow will define the setup for next week’s CPI.

What Moved Wall Street

Wednesday’s tape was defined by a geopolitical shock and a Fed minutes surprise landing in the same session. The Dow fell 1.1% to 52,348.39, its worst day in three weeks, after President Trump declared the ceasefire with Iran was over and Brent crude jumped nearly 7% intraday to above $79 before settling above $78. The S&P 500 slid 0.3% to 7,482.71, cushioned by chip strength, while the Nasdaq Composite bucked the tape entirely, adding 0.2% to 25,870.65 as Broadcom rose 4.8% on the expanded Apple US-components deal and Nvidia gained 3.6% on reports of higher H200 chip purchases from Chinese buyers.

The June FOMC minutes released at 2 PM ET showed a committee split down the middle. Several participants said they no longer view the current policy stance as restrictive, and a few actively made the case for raising rates. Ultimately the committee held rates steady at Chair Kevin Warsh’s first meeting at the helm, but the internal tone was more hawkish than markets had priced. That combination pushed the 10-year Treasury yield to 4.58%, a 4-week high, and hit rate-sensitive names hardest. Housing led losses. Builders FirstSource and PulteGroup both fell 5.4%, and D.R. Horton lost 4.6%. Credit-sensitive Dow names American Express down 3.8%, Sherwin-Williams down 3.5%, and Boeing down 3% rounded out the cyclical downdraft.

Assets in Focus

PepsiCo (PEP)

Reports Q2 2026 before the opening bell. Street consensus sits at $2.21 EPS on $23.95B revenue, implying roughly 5% revenue growth year over year. Analyst estimates have drifted lower, with EPS consensus down 1.3% over the past 30 days and revenue estimates hovering between $23.67B and $24.18B. North American snack volume is the key read for whether consumers are still absorbing Frito-Lay pricing or trading down. Coca-Cola’s cleaner recent execution has raised the comparison bar. Management guidance for the back half of 2026 will matter more than a narrow beat or miss on the headline number.

SK Hynix (KRX: 000660, ADR: SKHY)

Ripped 7.76% overnight to KRW 2.24 million ahead of Friday’s Nasdaq ADR debut. The book was oversubscribed more than 7x. Indicative ADR price of $165.26 implies a raise of approximately $29 billion, second only to SpaceX in US listing history and larger than Alibaba’s 2014 IPO or Saudi Aramco’s 2019 IPO. Anchor commitments include Baillie Gifford and Coatue. SK Hynix holds approximately 60% of the global HBM market and supplies Nvidia, Google, and Apple. The Nasdaq listing is expected to close the valuation gap versus Micron. SK Hynix currently trades at 6.2x forward earnings versus Micron at 7x.

Broadcom (AVGO)

Rose 4.8% Wednesday after expanding its agreement with Apple on US-made components. The move reinforces Broadcom’s role as one of the primary AI supply-chain beneficiaries and helped anchor the Nasdaq’s tape despite the cyclical selloff elsewhere.

Nvidia (NVDA)

Added 3.6% Wednesday on reports that Chinese firms plan to increase H200 chip purchases. Nvidia has again taken the role of tape-carrier every session where cyclicals sell off, and remains the single largest leadership stock heading into semi earnings season.

Micron (MU)

Fell 4.7% earlier in the week amid AI capex overspending worries but is set up as a natural read-through beneficiary of tomorrow’s SK Hynix Nasdaq debut. Any premium the SKHY ADR captures over its Korean-listed reference price would signal a broader re-rating for the memory basket.

Index Levels to Watch

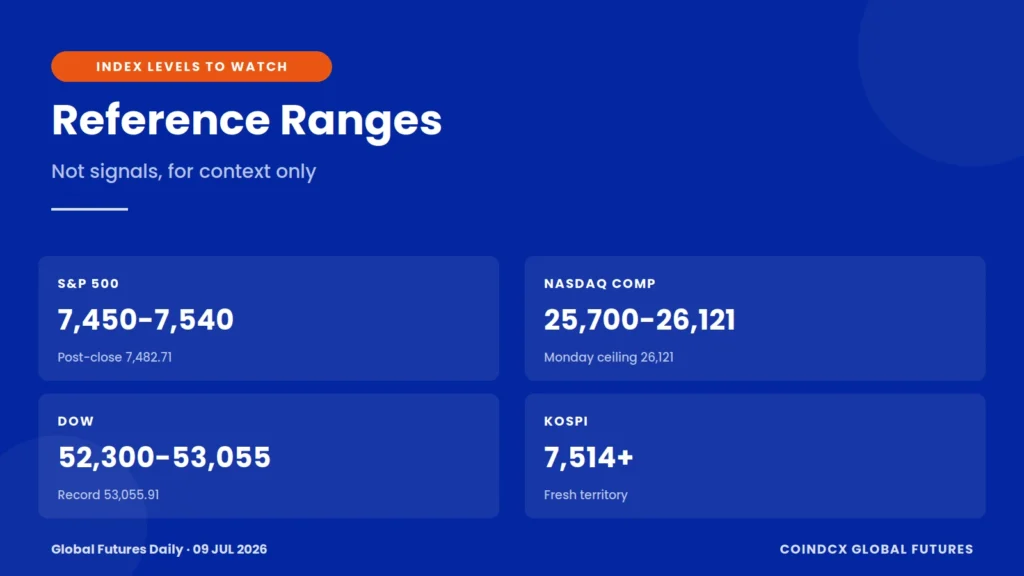

- S&P 500: closed 7,482.71 on Wednesday. Reference range 7,450 to 7,540, with the recent record area around 7,537.

- Nasdaq Composite: closed 25,870.65. Reference range 25,700 to 26,121, with Monday’s close of 26,121.16 as the near-term ceiling.

- Dow Jones: closed 52,348.39. Reference range 52,300 to 53,055, with July 6 record close of 53,055.91 as the upside marker.

- Russell 2000: hovering near 3,012, with cyclical proxy leadership under pressure.

- Kospi: closed 7,514.67 in fresh territory as the SK Hynix bid extends.

- Nikkei 225: closed 67,923.20, momentum extending on regional memory strength.

- 10-year Treasury yield: 4.58%, a 4-week high. This is the level rate-sensitive names are calibrating to.

- Brent crude: above $78 per barrel. WTI above $72 per barrel.

Disclaimer

This article is for educational and informational purposes only. It is not investment advice and should not be treated as a buy, sell, or hold recommendation for any security or financial product. Trading in futures and similar instruments involves significant risk including the potential loss of capital. Past performance is not indicative of future results.

Crypto products and NFTs are unregulated and can be highly risky. There may be no regulatory recourse for any loss from such transactions. For any queries, visit support.coindcx.com.

Frequently Asked Questions

Q1. What is the PepsiCo Q2 2026 consensus?

Street consensus is $2.21 EPS on $23.95B revenue, implying roughly 5% revenue growth year over year. Estimates have drifted 1.3% lower over the past 30 days. The Zacks consensus sits slightly lower at $2.19 EPS. PepsiCo reports before the opening bell.

Q2. Why did the Dow drop 1.1% on Wednesday?

President Trump declared the US-Iran ceasefire over following renewed strikes on both sides. Brent crude spiked nearly 7% intraday to above $79 before settling above $78, triggering rotation out of cyclical, rate-sensitive, and credit-sensitive Dow components. The June FOMC minutes released the same afternoon added pressure by revealing a Fed committee more open to rate hikes than markets had priced.

Q3. When does SK Hynix start trading on Nasdaq?

Friday, July 10, under the ticker SKHY. The offering is priced at an indicative $165.26 per ADR for a total raise of approximately $29 billion. That makes it the largest foreign ADR listing in Wall Street history, surpassing Alibaba in 2014 and Saudi Aramco in 2019, and second only to the SpaceX raise in June 2026 across all US listings. The book was oversubscribed more than 7x.

Q4. What did the June FOMC minutes reveal?

Several participants said they no longer view the current policy stance as restrictive, and a few actively made the case for raising rates at the June meeting. The committee ultimately held rates steady at Chair Kevin Warsh's first meeting, but the internal tone was more hawkish than markets had priced. Many participants also flagged persistent inflation pressures from tariffs, supply chain disruptions, and AI-related capital investment.

Q5. What are today's and tomorrow's key US catalysts?

Today: PepsiCo Q2 earnings before the opening bell, and weekly jobless claims at 8:30 AM ET. Tomorrow, Friday July 10: SK Hynix Nasdaq ADR listing goes live under ticker SKHY, and Delta Air Lines reports Q2 earnings. Next Tuesday, July 14: June CPI, the last major inflation read before the July 28 to 29 FOMC meeting.

{kind=link}

{kind=link}