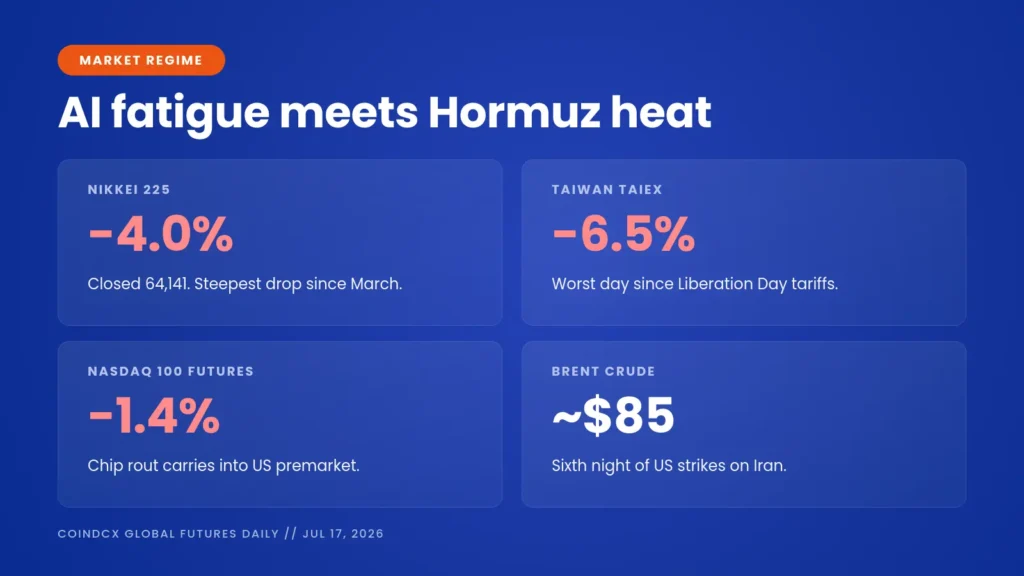

Asian chip rout deepened Friday with Nikkei down 4% and TAIEX -6.5% as Netflix Q3 guide missed. AXP, Travelers report; Brent near $85 on Iran strikes.

TLDR

The two-day post-CPI rally is over. Wall Street closed lower on Thursday as the semi complex extended its selloff even after TSMC posted a Q2 blowout, and the chip rout deepened overnight in Asia. Tokyo’s Nikkei 225 lost 4 percent to close at 64,141.12, its steepest one-day drop since March, and Taiwan’s TAIEX slid 6.5 percent – the worst session since Trump’s Liberation Day tariff move – with TSMC down 7.3 percent as investors punished the company’s raised $60-64B capex outlook. Netflix reported after the US close and Q2 was essentially in line, but the streamer’s Q3 revenue guide of $12.86B fell short of the $13B consensus and shares dropped over 8 percent in extended trading. US futures point lower with S&P 500 futures off 0.5 percent and Nasdaq 100 futures down 1.4 percent. At 8:30 AM ET the market gets June housing starts, building permits, and import/export prices; at 10 AM ET the University of Michigan preliminary July consumer sentiment reading. American Express, Travelers, Truist, and Fifth Third Bancorp report before the bell. The US carried out a sixth consecutive night of strikes on Iran with Brent crude rebounding toward $85 a barrel.

Market Regime

The tape has moved decisively from disinflation relief into AI-fatigue and geopolitical risk in the span of two sessions. On Wednesday, cool June PPI and megacap leadership pushed the S&P 500 to within 1 percent of its all-time high. On Thursday, the semiconductor complex started coming apart even after TSMC’s blowout, and now the position-clearing has spread across every major Asian market. Nikkei is down more than 13 percent from its recent peak. Taiwan’s TAIEX had its worst session in over a year. Japan’s Kioxia collapsed 16 percent and SoftBank shed 9 percent. The trigger is not one thing – it is the recognition that the AI capex cycle has become so large ($60-64B at TSMC alone) that any incremental raise starts to look like a margin worry rather than a demand tailwind.

Layered on top, Brent crude has retraced back toward $85 a barrel as the US carried out a sixth consecutive night of strikes on Iran. Two-year Treasury yields ticked higher on Thursday’s stronger-than-expected retail sales print, and hawkish comments from Fed officials have kept the September FOMC live even as the July hike has been priced back out. The setup into Friday’s US open is a market that has to absorb weak Asian handoff, a Netflix stock down 8 percent after hours, a fresh oil premium, and a light-touch data day of housing starts and Michigan sentiment. American Express earnings before the bell are the most important individual print of the session.

Bullish Factors

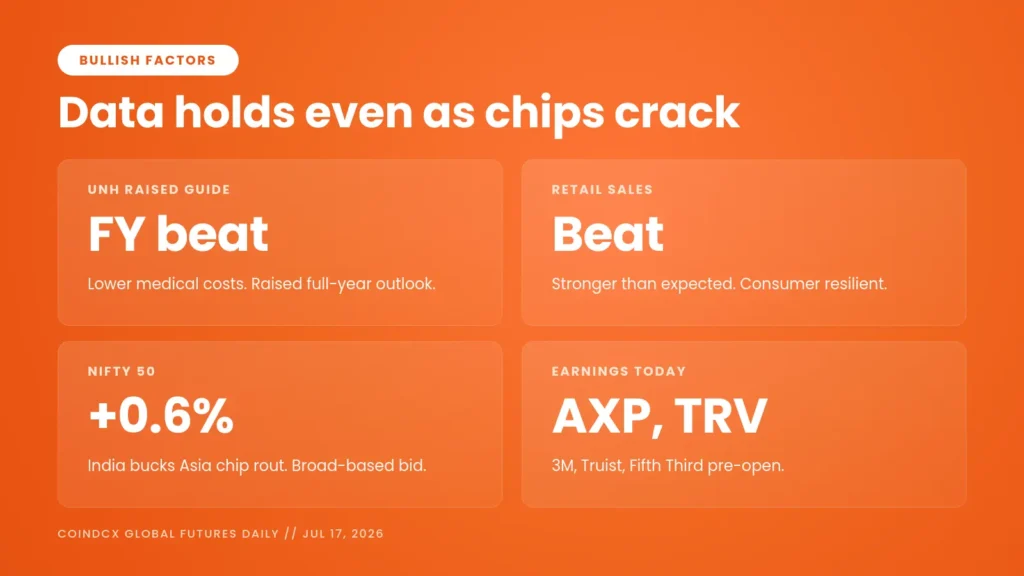

- Stronger June retail sales: The June print came in ahead of consensus, underscoring consumer resilience even as tech rolls over. That is the single biggest reason equity indices did not fall further on Thursday.

- UnitedHealth raised its full-year outlook: UNH beat Q2 estimates and raised full-year guidance on lower-than-expected medical cost trends, giving healthcare a fresh leg of leadership.

- Only two sectors closed red Thursday: The S&P 500 fell 0.51 percent but the damage was concentrated in Technology (-2.28 percent) and Communication (-0.63 percent). Healthcare, energy, and defensive sectors all traded higher on rotation.

- India Nifty 50 up 0.6 percent overnight: The Nifty bucked the broader Asian rout on domestic-consumption strength and the RBI’s June rate hold. India has become the cleanest positive-tape story in the region.

- Netflix Q2 revenue growth still 13.4 percent: Revenue of $12.56 billion versus $12.58 billion consensus is essentially in line, and top-line growth remains double-digit. The stock reaction is about the Q3 guide, not the underlying business trajectory.

- Rate expectations have not re-hardened: Cool CPI and PPI earlier in the week continue to anchor the July hike probability under 30 percent. Yields rising on Thursday reflect stronger data, not a hawkish repricing.

Bearish Factors

- Nikkei 225 down 4 percent, 13 percent off peak: Tokyo closed at 64,141 with Advantest -7.2 percent, Tokyo Electron -8.2 percent, SoftBank -9 percent, and Kioxia -16 percent. This is the steepest Nikkei drop since March.

- Taiwan TAIEX -6.5 percent: Worst session since April 2025. TSMC fell 7.3 percent even after the Q2 blowout as the raised $60-64B capex guide reignited margin concerns across the AI chain.

- Netflix -8 percent after hours: Q3 revenue guide of $12.86 billion undershot the $13 billion consensus. The company also announced it will move its “What We Watched” engagement report to annual publication, adding to opacity concerns.

- Brent crude toward $85: Sixth consecutive night of US strikes on Iran has kept the oil risk premium alive. Any material escalation feeds directly back into headline inflation.

- Nasdaq 100 futures -1.4 percent: European bourses set to open more than 1 percent lower. The overnight tape hands the US market a decisively risk-off open.

- Hang Seng Tech -5 percent: The Hong Kong tech gauge posted its sharpest one-day drop since April 2025 as the AI rerating spread from Taiwan and Tokyo into the China internet complex.

- Kospi closed for Constitution Day: South Korea is shut today, which means the Korean chip complex – which had led Monday’s early relief rally – cannot participate in either direction. Positioning imbalances risk amplifying next week.

Asian Markets This Morning

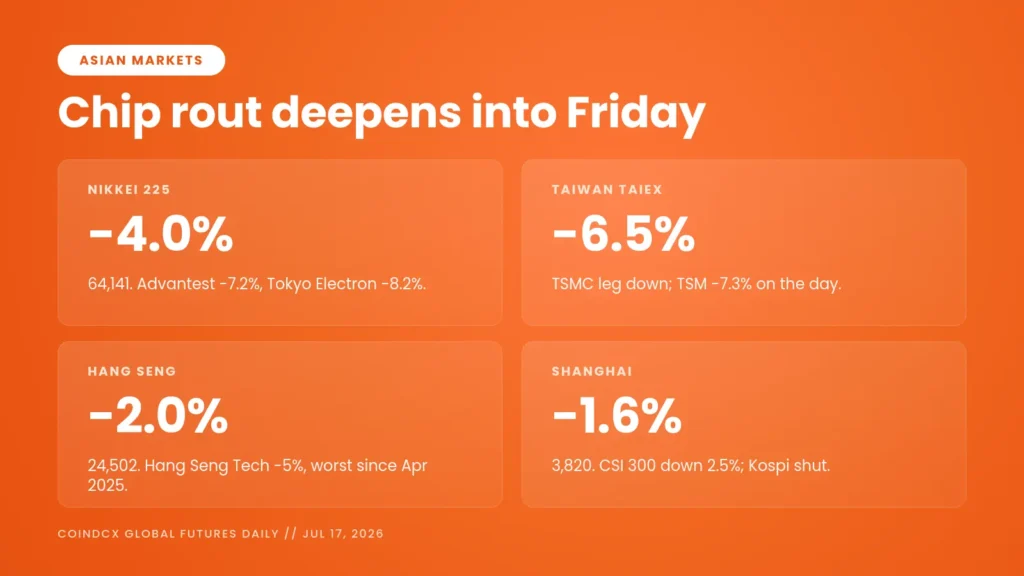

Every major Asian index outside India traded lower and the moves were sharp. Japan’s Nikkei 225 fell 4 percent to close at 64,141.12, its steepest one-day drop since March, and the broader Topix declined 2.6 percent. Chip-related names took the brunt: Advantest -7.2 percent, Tokyo Electron -8.2 percent, SoftBank Group -9 percent, and memory maker Kioxia collapsed 16 percent – a name that had briefly become Japan’s largest by market capitalization only weeks earlier. The Nikkei is now more than 13 percent below its recent peak.

Taiwan’s TAIEX fell 6.5 percent, its worst session since Trump’s Liberation Day tariff announcement, dragged down by a 7.3 percent decline in TSMC. Hong Kong’s Hang Seng lost 2 percent to close near 24,502 and the Hang Seng Tech Index dropped 5 percent – its sharpest single-day drop since April 2025. Mainland China’s Shanghai Composite slid 1.6 percent to 3,820 and the CSI 300 fell 2.5 percent. Australia’s ASX 200 and Singapore’s Straits Times each edged down about 0.5 percent. India’s Nifty 50 rose 0.6 percent, remaining the cleanest positive tape in the region. South Korean markets were closed for Constitution Day.

What Moved Wall Street Yesterday

The S&P 500 fell 0.51 percent to close at 7,533.77, the Nasdaq Composite dropped 1.47 percent to 25,881.95, the Dow Jones Industrial Average lost 105.67 points (or 0.20 percent) to 52,552.97, and the Russell 2000 was essentially flat at 2,974.57. It was a sector-driven session: only Technology (-2.28 percent) and Communication (-0.63 percent) closed lower, with every other sector modestly higher on rotation into healthcare, energy, and defensives. The 10-year Treasury yield rose 1.2 basis points to 4.557 percent as June retail sales came in stronger than expected.

TSMC dominated the tech story. The Taiwanese chip giant reported a 77 percent year-on-year profit surge for Q2 and raised full-year capital expenditure guidance to a $60-64 billion range from the prior $52-56 billion, along with committing an additional $100 billion to its Arizona chip footprint. Instead of lifting the sector, the print triggered a 4 percent decline in TSM ADRs and dragged the whole semiconductor complex lower. UnitedHealth was the other major mover on the upside, beating Q2 estimates and raising full-year guidance. Netflix reported after the close – Q2 in line at $12.56 billion revenue and $0.80 EPS – but Q3 revenue guidance of $12.86 billion versus the $13 billion consensus knocked the stock down over 8 percent in extended trading.

Assets in Focus

NFLX

Netflix Q2 revenue of $12.56 billion was fractionally below the $12.58 billion consensus, EPS of $0.80 was slightly above the $0.79 estimate, and net income came in at $3.4 billion. That is a clean in-line print. The problem was Q3 guidance of $12.86 billion versus a Wall Street bar closer to $13 billion, plus the announcement that the company will publish its “What We Watched” engagement report only annually starting in 2027 rather than semi-annually. Shares fell more than 8 percent in extended trading. The full-year revenue outlook was narrowed to $51-51.4 billion from the prior $50.7-51.7 billion range. The setup for the stock is difficult – engagement disclosure is being reduced just as the ad-tier ramp and live-sports monetization narrative needed a cleaner read.

TSMC / SMH

TSMC ADRs are set up for another leg down after the 7.3 percent drop in Taiwan. The trading implication is that raised capex guides across the AI chain – ASML earlier in the week, TSMC on Thursday – are being reinterpreted as a margin warning rather than a demand affirmation. That flips a positioning trade that had been long semiconductors for the last three quarters. The VanEck Semiconductor ETF (SMH) is the cleaner index-level read; watch the Monday session low as first support and the 25-day moving average below it as the second.

AXP

American Express reports before the open with consensus for Q2 EPS in the $4.20-4.30 range on approximately $18.7 billion in revenue. Focus items are cardholder spending trends after Wednesday’s retail-sales beat, credit performance in the T&E and small-business books, and any refresh to the full-year $17.30-17.90 EPS guide. AXP has been a consistent beat-and-raise name and a positive print is the single biggest offset the tape can get today against the chip and Netflix drag.

TRV / TFC / FITB

Travelers, Truist Financial, and Fifth Third Bancorp all report before the bell. Travelers is the read on P&C insurance rate adequacy heading into hurricane season. Truist and Fifth Third are the regional-bank follow-up to Tuesday’s big-bank beats – focus is on net interest margin trajectory, deposit costs, and any loan-loss provisioning changes. A clean sweep of beats in the regionals reinforces the financials leadership that has quietly persisted through the week’s tech turbulence.

NSDQ100

The Nasdaq 100 sits in a fresh technical zone. Thursday’s 1.6 percent drop combined with a 1.4 percent futures decline overnight puts the index into direct test of its 20-day moving average and Monday’s session low. First support is 25,600 (Monday intraday low); major support is 25,000 (the 50-day cluster). Resistance is 26,300, which now looks distant. The Netflix drag plus continued chip weakness makes a green open into the weekend the harder path.

XLE

Energy remains the mirror image of the risk trade. Brent rebounded toward $85 as the US carried out a sixth consecutive night of strikes on Iran. WTI followed. The sector has traded well every session that oil has printed positive, and a weekend of continued strikes plus the closed Kospi likely keeps XLE bid into Monday. Watch for any signal on the tape that ground deployment is on the table, which would take crude sharply higher and force a hawkish rethink from the Fed.

U MICH Sentiment

The University of Michigan preliminary July consumer sentiment print at 10 AM ET is the second consumer read of the week after Thursday’s retail sales beat. Consensus wants roughly 61-62 on the headline. A print above consensus with cooling 1-year inflation expectations is the cleanest possible confirmation of the disinflation-plus-consumer-resilience thesis and can offset some of the Netflix and chip drag.

Index Levels to Watch

S&P 500 (7,533.77 close)

- Immediate resistance: 7,600 (June record area)

- First support: 7,500 (round-number pivot, ~0.5 percent below close)

- Major support: 7,470 (June breakout retest, 50-day area)

Nasdaq Composite (25,881.95 close)

- Immediate resistance: 26,300 (recent range top, now distant)

- First support: 25,600 (Monday session low)

- Major support: 25,000 (psychological, 50-day cluster)

Nikkei 225 (64,141.12 close today)

- Immediate resistance: 66,000 (Thursday close area)

- First support: 64,000 (Friday close pivot)

- Major support: 62,500 (June lower channel)

Disclaimer

This article is for educational and informational purposes only. It is not investment advice and should not be treated as a buy, sell, or hold recommendation for any security or financial product. Trading in futures and similar instruments involves significant risk including the potential loss of capital. Past performance is not indicative of future results.

Crypto products and NFTs are unregulated and can be highly risky. There may be no regulatory recourse for any loss from such transactions. For any queries, visit support.coindcx.com.

Frequently Asked Questions

Q1. Why are Asian chip stocks falling so hard right after TSMC's blowout?

The Nikkei fell 4 percent to 64,141.12 and Taiwan's TAIEX dropped 6.5 percent with TSMC down 7.3 percent even after the company reported a 77 percent year-on-year profit surge in Q2 2026. The move reflects a rerating of the AI capex thesis: TSMC raised its 2026 capex guide to $60-64 billion from $52-56 billion and committed an additional $100 billion to its Arizona footprint. At current valuations across the semiconductor complex, that raise is being read as evidence that the industry needs to keep spending harder just to hold its position, which pressures long-term margins. Combined with ASML's earlier capex raise this week, the market is shifting from "AI demand affirmation" to "AI margin worry" as the operative frame.

Q2. What did Netflix report and why did the stock fall 8 percent?

Netflix reported Q2 revenue of $12.56 billion (versus $12.58 billion consensus), EPS of $0.80 (versus $0.79), and net income of $3.4 billion. That was essentially in line. The stock's after-hours drop was about the Q3 revenue guide of $12.86 billion, which fell short of the roughly $13 billion Wall Street had been expecting, plus the announcement that the company will move its "What We Watched" engagement report to annual publication starting in 2027 rather than the current semi-annual cadence. Reduced engagement disclosure at a time when the ad-tier ramp needs a clean read on user behavior was interpreted as opacity.

Q3. What US economic data comes out today?

At 8:30 AM ET (6:00 PM IST), the Census Bureau releases June housing starts and building permits, and the BLS releases June import and export prices. At 9:15 AM ET, the Federal Reserve releases June industrial production and capacity utilization. At 10:00 AM ET, the University of Michigan publishes its preliminary July consumer sentiment index. Consensus wants housing starts around 1.32 million SAAR, U Mich sentiment around 61-62, and industrial production essentially flat. Any material downside surprise on housing or sentiment would compound the risk-off tone.

Q4. What earnings are scheduled today?

Before the open: American Express (AXP), Travelers Companies (TRV), Truist Financial (TFC), Fifth Third Bancorp (FITB), and Regions Financial (RF). American Express is the most-watched name of the day for its read on consumer discretionary spending after Thursday's retail sales beat; the regional banks give the follow-up to Tuesday's big-bank prints on net interest margin trends and deposit costs; Travelers is the P&C insurance read into hurricane season. No major post-close reports.

Q5. What is happening with Iran and how is it affecting oil?

The US carried out a sixth consecutive night of strikes on Iran on Thursday, keeping the oil risk premium alive. Brent rebounded toward $85 a barrel and WTI followed. There has been no ceasefire since June and Trump has been briefed on options to expand the conflict, including additional bombing and potential ground deployment. As long as the strikes continue nightly, crude keeps a floor and the energy sector stays bid. Any material escalation - especially ground deployment - would push crude sharply higher and force a fresh look at Fed rate expectations, which have softened significantly after this week's cool CPI and PPI prints.

{kind=link}

{kind=link}