Samsung’s record Q2 profit couldn’t stop a global chip selloff as Kospi cracked 6% and SpaceX officially joined the Nasdaq-100 today.

TLDR

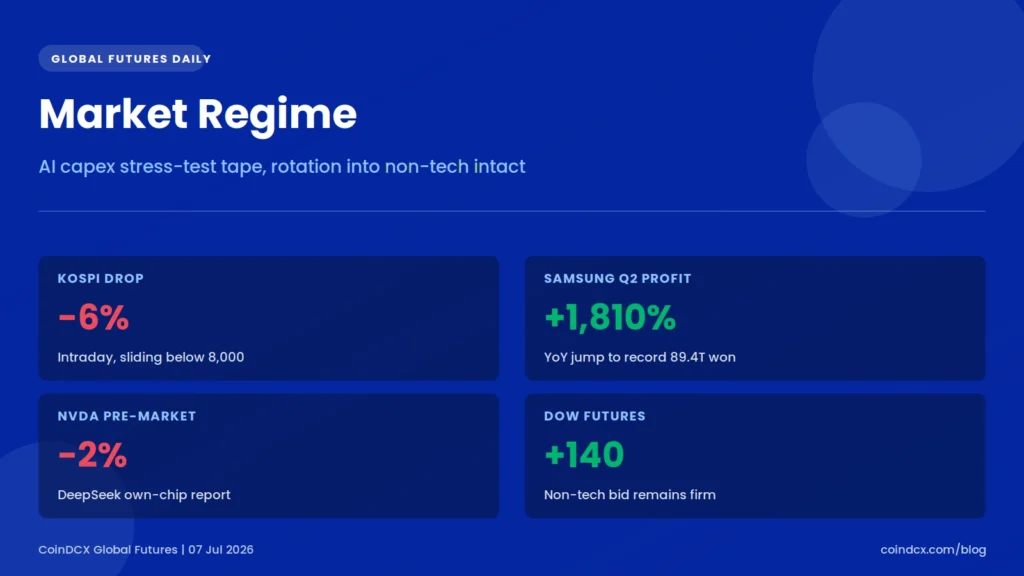

Samsung Electronics posted the largest quarterly operating profit in its history on Tuesday, an 89.4 trillion won print that beat consensus by nearly 3 trillion won and marked an 1,810 percent year-on-year jump. The stock still fell as much as 9.6 percent in Seoul, dragging the Kospi more than 6 percent below the 8,000 line and taking the entire Asia chip complex with it. Nikkei fell 2.12 percent, Tokyo Electron dropped over 4 percent, and the sell-the-news read was reinforced by a Reuters exclusive that DeepSeek is designing its own AI inference chip, sending Nvidia down about 2 percent in US pre-market. On the same morning, SpaceX officially joined the Nasdaq-100 before the open, with index funds already having triggered roughly 4.3 billion dollars in mechanical QQQ buying at Monday’s close. The FOMC minutes from the June 16 to 17 meeting land Wednesday at 2 PM ET.

Market Regime

The tape is fully in an AI capex stress-test regime. A record Samsung quarter that would normally be a green light for every chip name in the world instead triggered a global memory selloff, because the market is no longer pricing beat or miss, it is pricing what the capex line looks like in 2027 and 2028. Samsung guided to over 70 billion dollars in 2026 spend and analysts are now openly modelling AI overcapacity, with CXMT closing the gap in Chinese memory faster than expected.

Layered on top is a fresh Reuters scoop that DeepSeek is quietly building its own inference chip. Nvidia gave back its Monday bounce in pre-market. Yet the Dow is not participating in the selloff, futures are green there, which tells you the rotation into industrials, financials and defensives is still intact. SPCX joins the Nasdaq-100 at today’s open, which forces mechanical demand into one name even as the rest of the AI cohort bleeds. The setup into tomorrow’s FOMC minutes is a tape where Wall Street is stress-testing whether the AI leadership can absorb a supply and competition scare without breaking the broader rally.

Bullish Factors for Wall Street Today

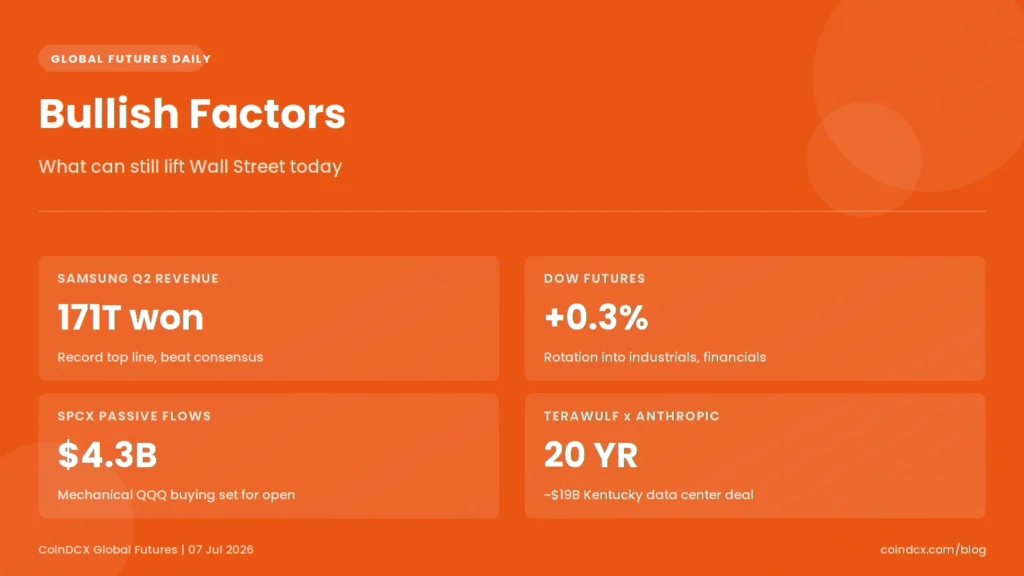

- Samsung’s 89.4 trillion won Q2 print is a real, cash-generative beat, not a hope trade. Revenue rose to 171 trillion won and full year 2026 is on track to exceed Samsung’s cumulative semiconductor profit of the past 40 years, according to guidance from DS division head Kim Yong-kwan.

- Dow futures were up around 140 points into the New York open, signalling that the pain is concentrated in AI-linked semis and not broad-based, with industrials, financials, healthcare and defensives absorbing rotation from tech.

- SPCX enters the Nasdaq-100 at today’s open with roughly 4.3 billion dollars in mechanical passive buying already priced in from Monday’s rebalance, per J.P. Morgan estimates. Historically, Nasdaq-100 additions have averaged 10 percent gains in the six months post-inclusion.

- Anthropic signed a 20-year, roughly 19 billion dollars data center deal with TeraWulf for a 400-megawatt Kentucky site, which is a fresh datapoint that hyperscaler compute demand has not peaked.

- RBC raised its Tesla price target to 500 dollars from 475, incorporating a potential SpaceX acquisition premium and lifting its robotaxi segment value by 20 percent on a higher global fleet forecast.

Bearish Factors for Wall Street Today

- Samsung shares fell as much as 9.6 percent in Seoul despite a record quarter, on capex and demand concerns and worries that Meta entering cloud infrastructure could distort hyperscaler demand. Analysts flagged that price beyond perfection was already in the stock.

- DeepSeek is developing its own inference AI chip, per Reuters, which would reduce its reliance on Nvidia and Huawei silicon. The report sent Nvidia down about 2 percent in US pre-market and adds a second Chinese competitor after Alibaba and Baidu also disclosed in-house chip programs.

- The Asia-Pacific memory complex broke down together. Kospi fell more than 6 percent intraday and below 8,000, Nikkei dropped 2.12 percent to 68,256.96, Advantest was off 2.76 percent, Tokyo Electron fell over 4 percent, Murata Manufacturing dropped 8.62 percent, and Taiwan’s Largan lost more than 6 percent.

- Micron traded 5 percent lower in US pre-market, with KLA, Marvell, Broadcom and AMD also lower. Nasdaq-100 futures were down about 0.9 percent, S&P 500 futures off 0.2 percent, indicating a concentrated tech-led open.

- Korean experts warn that CXMT is closing the memory technology gap with Samsung and SK Hynix faster than expected, and China’s DRAM push adds a supply overhang risk into 2027.

Asian Markets This Morning

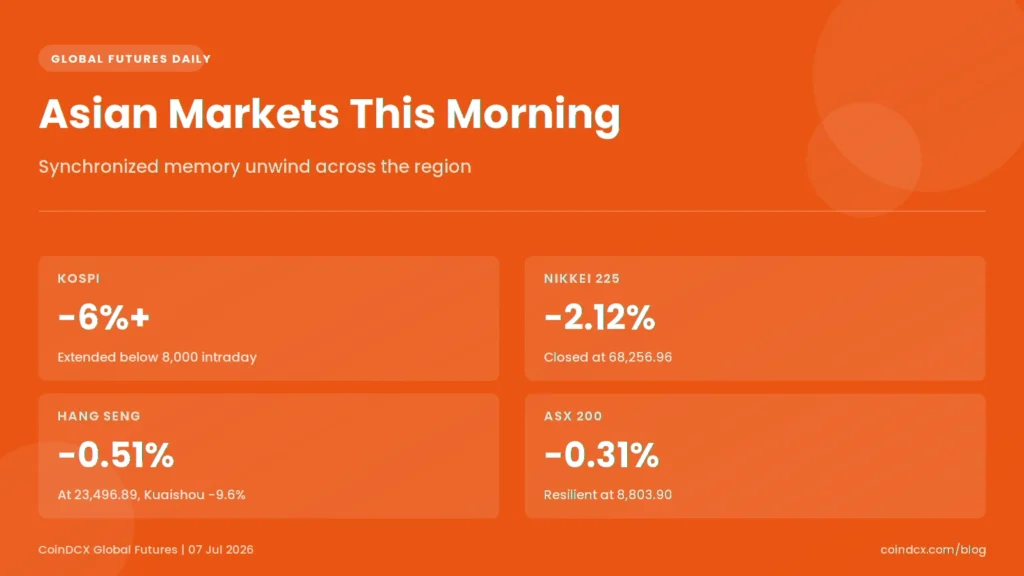

Asia was a synchronized memory unwind. South Korea’s Kospi opened down 1.64 percent at 7,919.20 and extended losses to more than 6 percent intraday, sliding into the 7,700s. Samsung Electronics fell as much as 9.6 percent, SK Hynix declined 1.45 percent to 2.309 million won, LG Energy Solution dropped 3.95 percent, Hyundai Motor dropped 3.19 percent, and Hanwha Ocean plunged over 20 percent after losing the Canadian submarine bid to ThyssenKrupp Marine Systems.

Japan’s Nikkei 225 fell 2.12 percent to 68,256.96, with the Topix down 0.97 percent to 4,062.26. Tokyo Electron was off more than 4 percent, Murata Manufacturing dropped 8.62 percent, SoftBank fell over 4 percent, and Fanuc lost 5.44 percent. Hong Kong’s Hang Seng slipped 0.51 percent to 23,496.89, dragged partly by Kuaishou which fell 9.6 percent after Tencent sold a 1.5 billion dollars stake at a 6 percent discount. Mainland China’s CSI 300 dropped 1.03 percent to 4,792.26. Taiwan’s TSMC eased 0.81 percent, Hon Hai fell 2.27 percent, and Largan dropped over 6 percent. Australia’s ASX 200 held up better, down only 0.31 percent to 8,803.90 given limited semiconductor supply chain exposure.

What Moved Wall Street Yesterday

Monday was a broad-based melt-up on the first trading session after the July 4 holiday. The Dow gained 155.84 points, or 0.29 percent, to close at 53,055.91, the first close ever above 53,000. The S&P 500 rose 0.72 percent to 7,537.43, and the Nasdaq Composite added 1.12 percent to 26,121.16. Semiconductor momentum led the advance, with the VanEck Semiconductor ETF (SMH) up around 2 percent after two down weeks.

Anthropic signed a 20-year deal to use TeraWulf’s 400-megawatt Kentucky data center, worth over 19 billion dollars across the initial term, and TeraWulf shares jumped over 16 percent. ASML rose 4 percent after Bernstein raised its price target more than 30 percent to 2,300 dollars. Intel gained about 3 percent to 123.98 dollars on targeted CPU price hikes. Astera Labs surged 10.5 percent after Bank of America raised its price target to 450 dollars. Dell jumped 7.7 percent after President Trump publicly promoted its computers from the White House. Vertex Pharmaceuticals agreed to buy Crinetics for 10 billion dollars, and Crinetics shares nearly doubled after the close.

Assets in Focus

NVDA

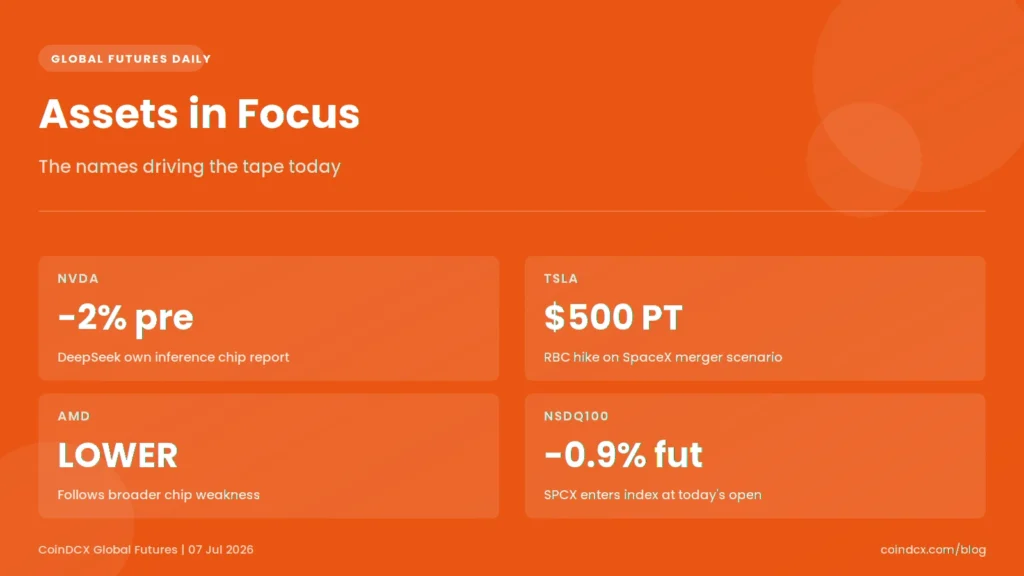

Nvidia was down about 2 percent in US pre-market after Reuters reported that DeepSeek is developing its own AI inference chip, marking the second high-profile Chinese customer to move toward in-house silicon after Alibaba and Baidu. The chip is designed for inference workloads and is still in early stages, with DeepSeek in discussions with foundries and memory suppliers. This is a reference point for context, not an entry or exit signal.

TSLA

RBC Capital raised its Tesla price target to 500 dollars from 475, embedding a 25 to 30 percent premium tied to a potential SpaceX acquisition scenario and lifting the robotaxi segment valuation by 20 percent on a higher global fleet forecast. Excluding any SpaceX premium, RBC pegs Tesla’s intrinsic value at 435 dollars per share. TSLA was indicated higher in pre-market.

AMD

AMD traded lower in US pre-market alongside the broader memory and semiconductor cohort as investors reassessed AI capex forecasts after Samsung’s sell-the-news reaction. No single-name catalyst on AMD today, but any softening in inference-chip demand narratives from DeepSeek carries direct read-through to AMD’s MI series accelerator roadmap.

NSDQ100

Nasdaq-100 futures were down about 0.9 percent into today’s open as chip weakness dominated pre-market flow. SPCX officially joins the index before today’s open with a weighting below 1 percent, following about 4.3 billion dollars in mechanical passive buying triggered at Monday’s close. Historically, additions have gained an average 10 percent in the six months post-inclusion and 18 percent in the twelve months, per Motley Fool data on the last decade of Nasdaq-100 entrants.

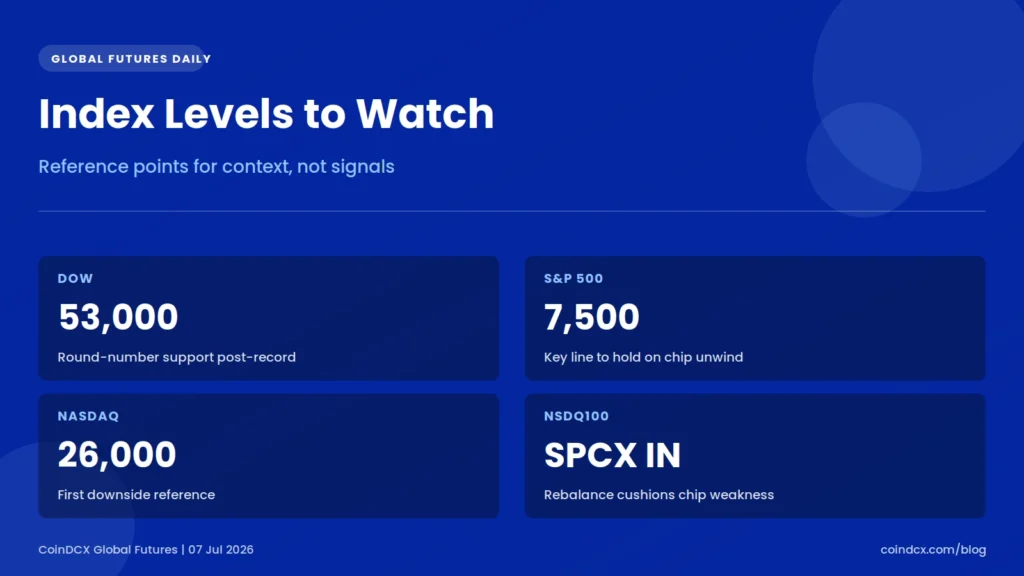

Index Levels to Watch

- Dow Jones Industrial Average: closed at 53,055.91 on Monday, first ever close above 53,000. Round-number 53,000 becomes near-term support, 52,742 was the recent intraday reference from July 1.

- S&P 500: closed at 7,537.43. Watching whether the index can hold above 7,500 during the chip unwind, with 7,483 as reference support from July 1.

- Nasdaq Composite: closed at 26,121.16. First test is whether the index defends 26,000 into today’s tech-led open.

- Nasdaq-100: futures pointing to a roughly 0.9 percent lower open. Index adds SPCX today and the rebalance flow could partially cushion the chip selloff, though the net impact hinges on whether SPCX holds its Monday close.

Disclaimer

This article is for educational and informational purposes only. It is not investment advice and should not be treated as a buy, sell, or hold recommendation for any security or financial product. Trading in futures and similar instruments involves significant risk including the potential loss of capital. Past performance is not indicative of future results.

Crypto products and NFTs are unregulated and can be highly risky. There may be no regulatory recourse for any loss from such transactions. For any queries, visit support.coindcx.com.

Frequently Asked Questions

Q1. Why did Samsung's stock fall despite record Q2 earnings?

Samsung reported preliminary Q2 operating profit of 89.4 trillion won, an 1,810 percent year-on-year jump and above the 87.3 trillion won LSEG consensus. Shares still fell as much as 9.6 percent because the market had already priced a historic quarter, and investors focused on rising capex, potential AI overcapacity signals, and Meta's move into cloud infrastructure that could reshape hyperscaler memory demand.

Q2. When does SpaceX officially join the Nasdaq-100?

SPCX joined the Nasdaq-100 before the open on Tuesday, July 7, 2026. Index-tracking funds had already begun purchasing shares at Monday's closing price to reflect the rebalance, with J.P. Morgan estimating about 4.3 billion dollars in mechanical passive inflows. SPCX enters at a weight below 1 percent.

Q3. What is the DeepSeek chip news and why does it matter for Nvidia?

Reuters reported on July 7 that Chinese AI startup DeepSeek is developing its own AI inference chip in discussions with foundries and memory suppliers. If successful, this reduces DeepSeek's dependence on Nvidia and Huawei silicon. Nvidia fell about 2 percent in US pre-market on the report, since inference is the fastest-growing corner of AI compute demand and losing a marquee Chinese customer would extend the pressure from Alibaba and Baidu's in-house programs.

Q4. What are the key US catalysts this week?

FOMC minutes from the June 16 to 17 meeting are due Wednesday, July 8 at 2 PM ET. The June CPI print lands the following Tuesday, July 14, and is the last inflation read before the July 28 to 29 FOMC meeting. SK Hynix's Nasdaq American Depositary Receipt listing goes live on July 10.

{kind=link}

{kind=link}