SpaceX (SPCX) joins the Nasdaq-100 Tuesday, triggering $4.3B in QQQ buying as Wall Street reopens with tech futures up 1.1% on Foxconn’s 40% Q2 revenue jump.

TLDR

- US markets reopen Monday after the July 3 Independence Day observed holiday, with Nasdaq-100 futures up 1.1% and S&P 500 futures up 0.5% pre-market, led by chip stocks.

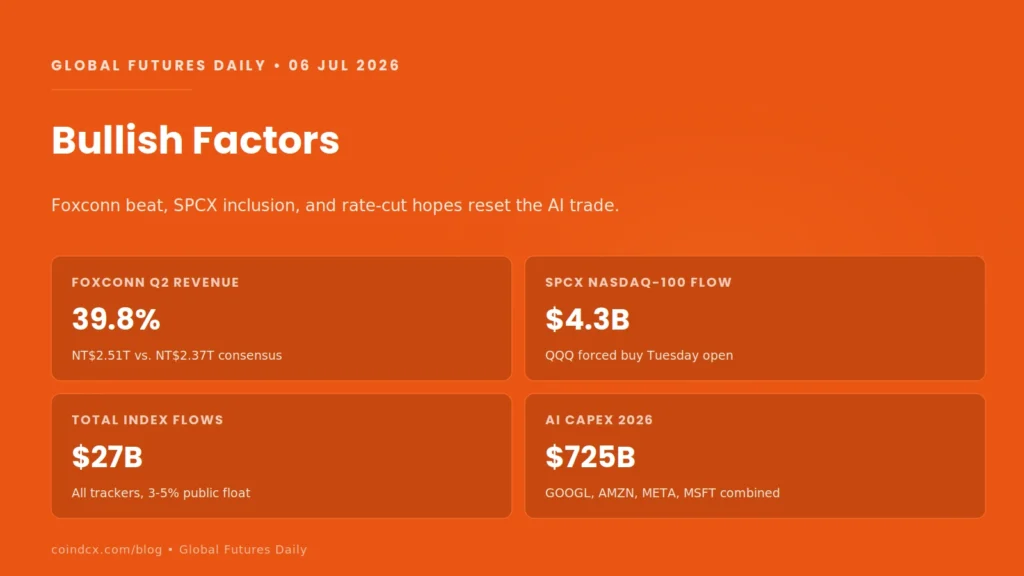

- Foxconn Q2 revenue jumped 39.8% year on year to NT$2.51 trillion (~$79 billion), beating the NT$2.37 trillion consensus, with AI rack shipments guided to keep growing in Q3.

- SpaceX (SPCX) officially joins the Nasdaq-100 before market open on Tuesday July 7, with roughly $4.3 billion in forced QQQ buying and up to $27 billion in total index flows into a 3 to 5 percent float.

- Today’s US data catalyst is the June ISM Services PMI at 10:00 AM ET, moved from the usual third business day slot due to the holiday.

- Samsung Electronics is expected to release Q2 preliminary earnings guidance on Tuesday, July 7, a key memory-chip read for the AI trade.

- Wednesday delivers FOMC Minutes from the June 16 to 17 meeting, followed by June CPI on July 14 as the next macro milestones.

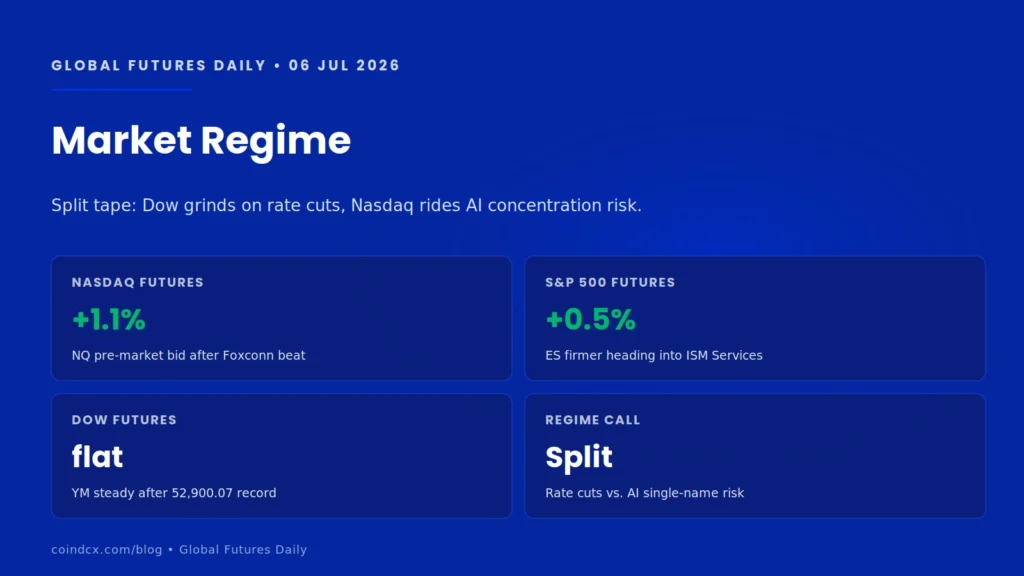

Market Regime

Wall Street returns from the extended weekend with the tech bid firmly back on. After last week’s chip rout that hit Micron 19% and dragged the Nasdaq lower even as the Dow set a fresh record at 52,900.07, the AI trade has caught a Sunday-night lifeline from Nvidia’s largest server assembly partner. Foxconn’s blowout Q2 print flipped positioning heading into a week loaded with the SPCX Nasdaq-100 rebalance, Samsung’s memory read, and Wednesday’s FOMC Minutes.

The regime remains split. The Dow and S&P 500 keep grinding on rate-cut expectations that firmed after last Thursday’s 57K NFP miss, while the Nasdaq is a story of concentration risk where a single AI catalyst can move the whole tape. What could break it: any sign in this morning’s ISM Services print that the prices index is holding above 71 for a second straight month, which would put the July 29 FOMC decision back in play as a live meeting.

Bullish Factors

- Foxconn Q2 revenue up 39.8% YoY to NT$2.51 trillion, above NT$2.37 trillion consensus, with AI rack shipments guided to keep growing in Q3.

- $725 billion in combined 2026 AI capex from Alphabet, Amazon, Meta, and Microsoft, with Goldman flagging a potential $1.4 trillion by 2027.

- SPCX Nasdaq-100 inclusion Tuesday triggers ~$4.3 billion in QQQ buying and up to $27 billion in total forced index flows against a 3 to 5 percent public float.

- June ISM Manufacturing PMI held expansion at 53.3, the 21st month above 50 despite easing from 54.0 in May.

- Dow closed Thursday at a record 52,900.07, up 1.14%, on rate-cut expectations that firmed after the NFP miss.

- Bank of America upgraded India’s reform momentum as a structural shift over the weekend; Nifty 50 opened +0.5%, rupee steady at 95.23.

Bearish Factors

- June NFP came in at +57K versus +110K expected, with the April and May revisions taking off a combined 74K, questioning labor market resilience.

- Late-June semi rout still fresh in positioning: MU -19% on the week, SMH -4.5% Thursday, Teradyne -13.6%.

- Tesla fell 7.5% Thursday to $393.45 despite record Q2 deliveries of 480,126, a reminder that valuation sensitivity cuts both ways on beats.

- Samsung Electronics and SK Hynix fell 4.7% and 3.1% respectively last week on reports of $1 trillion-plus AI investment plans reviving capex-cycle fears.

- Kospi -0.46% and Kosdaq -2.46% Monday, showing Asia’s AI enthusiasm has near-term limits despite the Foxconn beat.

- ISM Services prices index at 71.3 in May, the highest since August 2022, keeps sticky services inflation as a Fed-pause risk into this morning’s June print.

Asian Markets This Morning

- Japan Nikkei 225 little changed at 69,737.69; Topix +0.92% to 4,101.96, showing broader-market strength beneath a flat headline.

- South Korea Kospi -0.46% to 8,051.33; Kosdaq tumbled 2.46% to 847.07 on small-cap tech unwind.

- Australia S&P/ASX 200 -0.15% to 8,831.00 in a quiet holiday-thinned session.

- China CSI 300 flat at 4,842; Hong Kong Hang Seng last +0.81%, extending a China AI rotation call from Quantum Strategy.

- India Nifty 50 +0.5% in early trade; rupee steady at 95.23 vs. USD.

- Foxconn’s Sunday print set the risk-on tone for the Asia session before US futures caught the bid.

What Moved Wall Street Last Session

- Dow closed Thursday, July 2, at a record 52,900.07, up 1.14%, driven by rate-cut hopes following the June NFP miss.

- S&P 500 slightly negative and Nasdaq Composite lower on a broad semiconductor sector rout.

- Tesla -7.5% to $393.45 on a sell-the-news reaction to record Q2 deliveries of 480,126 (+25% YoY).

- Netflix +5% ahead of its confirmed July 16 earnings; Meta -5% after the market processed its cloud business launch.

- SMH -4.5% and Teradyne -13.6% led the chip decline; the 2-year yield dropped 3.5 bp after the payrolls miss.

- Kroger and Giant Eagle sealed a $1.65 billion acquisition, while Fed Chair Warsh’s Sintra remarks kept a neutral tone on monetary policy.

Assets in Focus

- NVDA: Foxconn’s beat is a direct AI capex signal; watch for spillover into the Nasdaq-100 open. Last close $194.84 (-1.4%) on Thursday.

- TSLA: Thursday close $393.45 (-7.5%). After record deliveries, the July 22 Q2 earnings is the next real valuation test.

- SPCX: Nasdaq-100 inclusion before Tuesday July 7 open, currently in the $149 to $163 range. Q2 earnings August 6 opens the first insider lockup window.

- AAPL: Foxconn assembly volumes signal iPhone 17 supply outlook. Last close $308.74 (+4.9%). Q2 earnings confirmed for July 30 AMC.

- META: Down 5% Thursday on cloud-business launch reception. Q2 earnings likely July 29 AMC.

- MSFT and AMZN: Q2 earnings likely July 29 and July 30 AMC respectively, bookending the FOMC + BoJ vol window.

- GOOGL: Q2 earnings confirmed for July 28 AMC. The Berkshire $10B private placement and the $84.75B equity capital raise remain overhangs into the print.

- NFLX: Confirmed July 16 AMC earnings, with the +5% Thursday move suggesting positioning is already tilting long.

Index Levels to Watch

- Dow (YM): 53,000 is the psychological breakout level; the July 2 record close was 52,900.07.

- S&P 500 (ES): 7,483.23 last close, with 7,500 as the next round-number resistance.

- Nasdaq (NQ): 26,040.03 last close, 26,500 as the trend extension if the AI bid holds.

- Russell 2000: 3,012.59 last close, 3,000 as the near-term support to defend.

- DXY: Dollar softened after the NFP miss; watch the 96 handle as a break level.

- WTI: Around $70 per barrel, holding above key support in the post-Iran-ceasefire regime.

Disclaimer

This article is for educational and informational purposes only. It is not investment advice and should not be treated as a buy, sell, or hold recommendation for any security or financial product. Trading in futures and similar instruments involves significant risk including the potential loss of capital. Past performance is not indicative of future results.

Crypto products and NFTs are unregulated and can be highly risky. There may be no regulatory recourse for any loss from such transactions. For any queries, visit support.coindcx.com.

Frequently Asked Questions

Q1. Why are US markets closed only on Friday, July 3, 2026?

The NYSE and Nasdaq observed Independence Day on Friday, July 3, since July 4 fell on a Saturday. Bond markets were also shut for the day. Regular trading resumed Monday July 6.

Q2. What is the SPCX Nasdaq-100 inclusion and why does it matter?

SpaceX joins the Nasdaq-100 before market open on Tuesday, July 7, just 15 trading days after its June 12 IPO. That is the fastest addition ever under Nasdaq's updated inclusion rules. Passive index funds tracking the Nasdaq-100 will need to buy roughly $4.3 billion in SPCX from QQQ alone, with up to $27 billion across all index-tracking products. Because only 3 to 5 percent of shares are in public float, the inflow creates a mechanical supply-demand squeeze.

Q3. What did Foxconn's Q2 print mean for the AI trade?

Foxconn (Hon Hai Precision), the largest server assembler for Nvidia, reported NT$2.51 trillion ($79 billion) in Q2 revenue on Sunday, up 39.8% YoY and well above the NT$2.37 trillion consensus. The company guided AI rack shipments to keep growing in Q3, which reset positioning after last week's chip rout.

Q4. What US data is out today?

The June ISM Services PMI at 10:00 AM ET is the day's key US print, moved from its usual third-business-day slot due to the July 3 holiday. May's Services PMI came in at 54.5 with the prices index at 71.3, the highest since August 2022.

Q5. When is Samsung Electronics Q2 preliminary guidance?

Samsung is expected to release its Q2 preliminary earnings guidance on Tuesday, July 7, a critical read on memory chip pricing and AI demand ahead of the SPCX Nasdaq-100 inclusion the same morning.

Q6. What was the June NFP print and why did it move markets?

US nonfarm payrolls came in at +57K in June against expectations of +110K, with April and May revised down by a combined 74K. The unemployment rate held at 4.2%. The miss shifted rate-cut expectations for the July 29 FOMC decision and drove the Dow to its 52,900.07 record close, while pressuring semis on growth concerns.

{kind=link}

{kind=link}