SK Hynix filed a $29 billion Nasdaq IPO as SKHY on June 30, with trading set for July 10. Wall Street closed a historic H1 with Nasdaq up 12.8% and Russell 2000 up 21.8%. ADP and ISM Manufacturing land today.

Key takeaway

The largest AI memory play in global chip markets just filed to trade on Nasdaq. On June 30, SK Hynix submitted its Form F-1 to the SEC under the ticker SKHY, targeting a raise of up to 29.4 billion dollars, a listing that could rank among the five largest share sales in history and sit near the scale of Saudi Aramco 2019. Trading is set to begin July 10 with subscription on July 14. The filing closes a first half that already broke records for US equities: Dow up 8.9 percent, S&P 500 up 9.6 percent, Nasdaq up 12.8 percent, Russell 2000 up close to 22 percent for its best first half since 1991. Second half opens on a more cautious note. US futures slipped early Wednesday, the yen cracked a fresh 40 year low near 162.67, and traders are looking at ADP and ISM Manufacturing today before Thursday brings the June nonfarm payrolls report in a holiday shortened week.

Market regime

The tape closes the first half in a risk-on but stretched posture. Every major US benchmark logged a positive H1, with Nasdaq’s plus 12.8 percent leading on the back of a plus 19.6 percent second quarter, its strongest three months since Q2 2020. The Dow’s plus 8.9 percent is its best first half since 2021, and the Russell 2000’s near plus 22 percent is the standout, the broadest first half signal since 1991 that the rally is finally reaching beyond mega-cap tech. But the second half opens with visible wobble points. The yen has cracked to a fresh 40-year low near 162.67 versus the dollar, raising Bank of Japan intervention risk. Oil finished Q2 down close to 30 percent for WTI and gold posted its worst quarter since Q2 2013, both signalling a safe-haven rotation into risk that is already crowded. Positioning remains long tech, long small caps, and long US dollar, which makes the next two prints, ADP today and NFP Thursday, the pivot points that decide whether H2 opens with a squeeze or a shakeout.

Bullish factors

- SK Hynix Nasdaq listing filed under SKHY, a direct high bandwidth memory and AI chip play landing July 10, first HBM leader on US markets alongside Micron

- CME Group announced single stock futures on 50 plus US names launching July 27, including NVDA, TSLA, AAPL, SPCX, and MU

- Nasdaq books its best quarter since Q2 2020 at plus 19.6 percent

- Russell 2000 posts its best first half since 1991 at close to plus 22 percent, signalling the rally is broadening beyond mega cap tech

- Iran and US ceasefire is holding, Strait of Hormuz commercial traffic normalised

- AMD tagged a fresh record high on Morgan Stanley calls around the Venice sixth generation CPU roadmap

Bearish factors

- Yen at a 40 year low near 162.67 versus dollar, raising the odds of Bank of Japan intervention and a carry trade unwind that could hit AI positioning

- WTI crude down close to 30 percent for the quarter and 19 percent for the month, energy names remain under pressure

- Gold posted its worst quarter since Q2 2013, signalling that the safe haven rotation into risk assets is already stretched

- Nike Greater China revenue fell 12 percent year on year, weighing on the consumer discretionary read

- ISM services employment sub index has now contracted for three straight months, an early crack in the labour market

- Japan 30 year JGB yield sitting near 4 percent, building global duration risk

- A strong ADP or NFP print this week could push Fed July hike odds higher and lift real yields

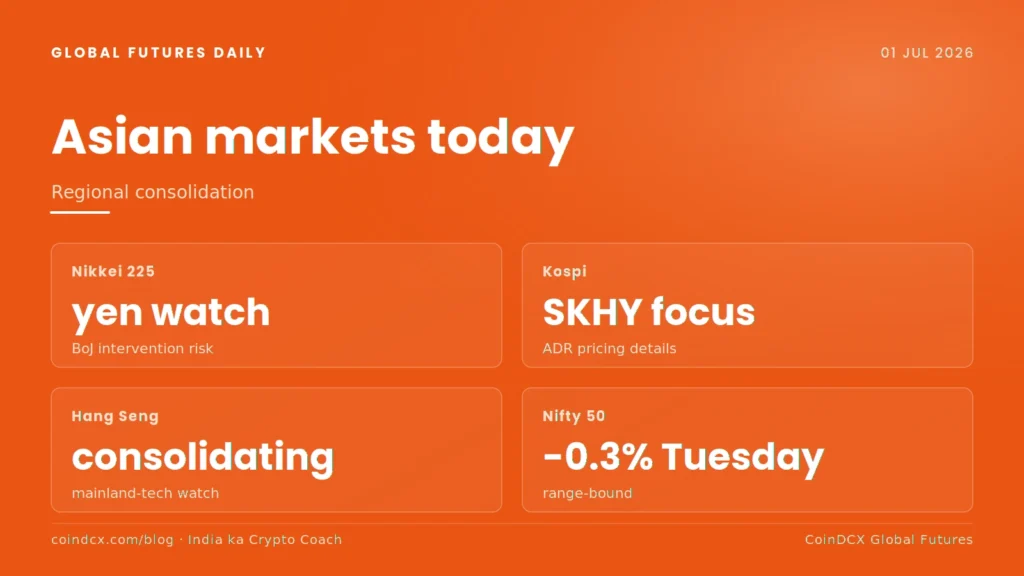

Asian markets this morning

- Nikkei 225: opened weaker after a plus 0.9 percent Tuesday close, yen weakness supports exporters but pressures the Bank of Japan credibility trade

- Kospi: consolidating after Tuesday plus 1 percent close, SK Hynix ADR pricing details are the local focus

- Hang Seng: soft Tuesday close at minus 0.6 percent, watching mainland tech follow through into H2

- Nifty 50: minus 0.3 percent Tuesday, continuing the near term consolidation pattern

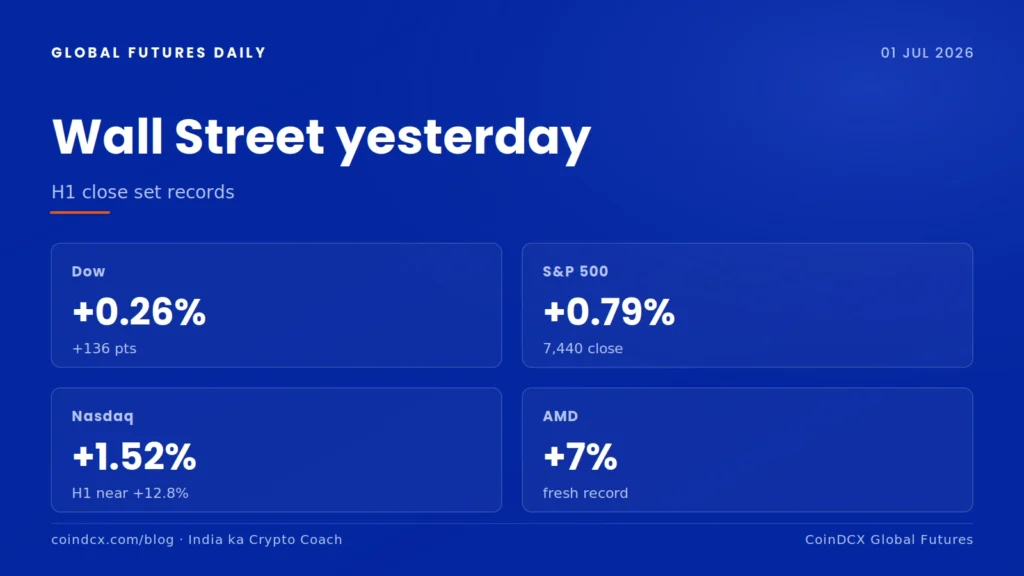

What moved Wall Street yesterday

- Dow: plus 136 points or plus 0.26 percent to close the first half near a record

- S&P 500: plus 0.79 percent

- Nasdaq: plus 1.52 percent

- SK Hynix F-1 filing hit the tape late morning ET and quickly reset the AI supply chain conversation

- CME single stock futures announcement added a structural bid to the listed names on its roster

- AMD closed plus 7 percent at a record high on Venice roadmap chatter

- Nike closed lower after the Greater China revenue miss

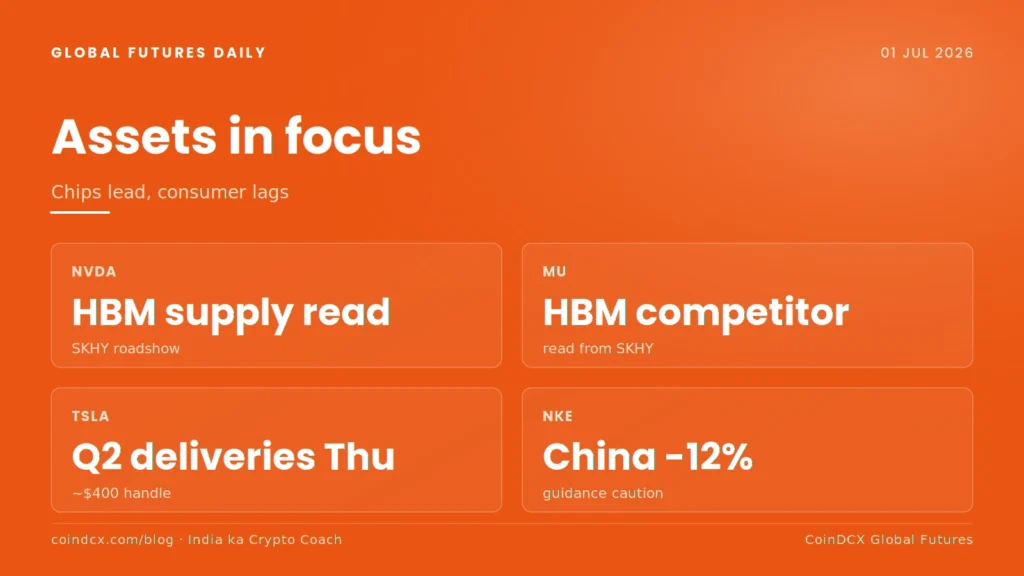

Assets in focus

- NVDA: HBM supply chain read from the SKHY filing. Watch the reaction to SKHY roadshow feedback.

- AMD: Venice CPU roadmap follow through after a plus 7 percent record close. Prior day high is the reference to hold.

- MU: Direct HBM competitor read from SKHY. HBM pricing power and share dynamics are the key watch.

- TSLA: Q2 deliveries drop Thursday. Morgan Stanley raised estimates. The 400 dollar handle is the level in play.

- NKE: Greater China revenue minus 12 percent and guidance caution. Post-earnings low is the level to monitor.

- NSDQ100: Best quarter since 2020 delivered. Mean reversion risk on the H2 open around the 30,050 area.

Index levels to watch

- Nasdaq 100 futures: 30,050 area into the second half open, first meaningful support cluster around 29,700

- S&P 500 futures: 7,440 close as base, resistance clusters around 7,470

- Russell 2000: 3,026 futures print, bullish structure intact above 2,960

- Dollar index (DXY): 101.16, the yen side of the trade is the trigger to watch

Today’s catalysts (IST)

- 4:45 PM: ADP Non-Farm Employment Change, forecast plus 118K, prior plus 122K

- 6:30 PM: ISM Manufacturing PMI, forecast 53.8, prior 54.0

- 6:30 PM: Construction spending, forecast plus 0.1 percent

- 7:00 PM: EIA weekly crude oil inventories, forecast minus 4.8 million barrels

- Ongoing: SK Hynix ADR roadshow investor feedback

Disclaimer

This article is for informational purposes only and is not investment advice. Trading in US Stock Futures, crypto assets, and other instruments carries risk including the potential loss of principal. CoinDCX does not provide trade recommendations and the price levels referenced are context points, not entry or exit signals. Crypto products and Virtual Digital Assets (VDA) are unregulated and can be highly risky. There may be no regulatory recourse for any loss from such transactions. For any queries, visit support.coindcx.com

{kind=link}

{kind=link}