Tesla Q2 deliveries and June NFP both drop Thursday as Wall Street braces for a double-catalyst session before Friday’s July 4 close. Nasdaq -0.66%.

TLDR

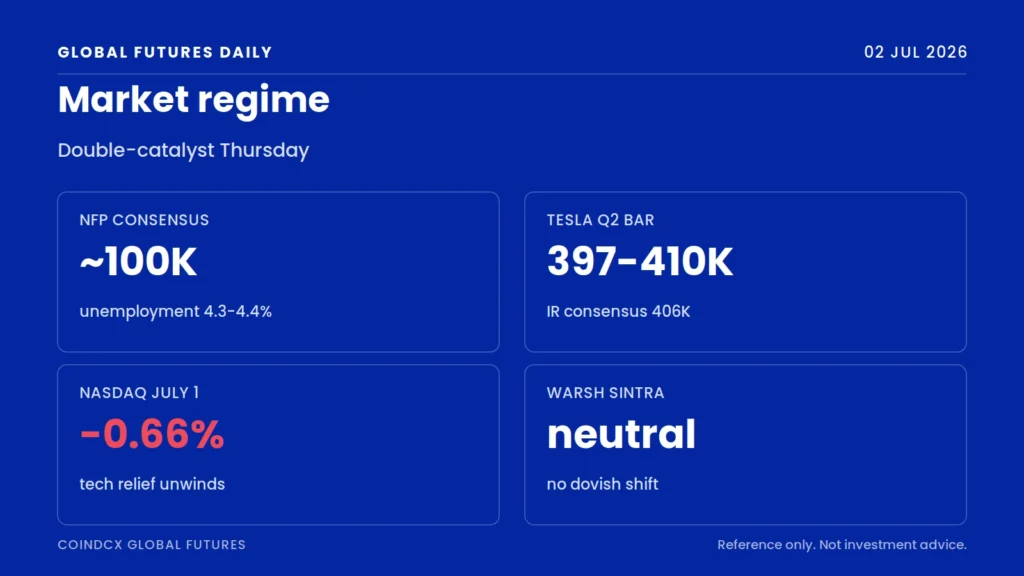

Two independent catalysts land in the same session. Tesla Q2 delivery numbers drop today, with the company’s own investor-relations consensus at 406,024 vehicles and Bloomberg at ~397,000. It is the first hard read on whether the 50,000-unit inventory build in Q1 was tax-credit turbulence or a genuine demand ceiling. June nonfarm payrolls also print today at 6:00 PM IST, moved forward one session because US markets close Friday for Independence Day. Consensus is roughly 100K jobs, unemployment at 4.3 to 4.4 percent, and average hourly earnings +0.3 percent month-over-month. Q3 opened Wednesday with the two-day tech relief rally coming undone: Nasdaq -0.66 percent, S&P 500 -0.22 percent, Dow essentially flat at 52,305. Fed Chair Kevin Warsh spoke at the ECB Sintra Forum but stayed neutral on forward guidance, and ADP’s 98K private payrolls print undershot the ~115K consensus, adding to the case that today’s headline number could show the labor market cooling faster than the Fed’s July path assumes.

Market Regime

The tape opened Q3 unwinding the sharp two-day rally that closed Q2, with technology giving back leadership as investors trimmed exposure ahead of a double-catalyst Thursday. This is a data-driven session where a hot NFP print above 130K reinforces Warsh’s no-cuts-this-year positioning and pressures long-duration tech, while a soft print below 80K reopens the September rate cut trade and lifts small caps and rate-sensitive sectors. Layered on top, Tesla’s Q2 delivery number gives the market its first hard read on whether the Q1 inventory build was one-off tax-credit turbulence or the start of a demand ceiling. The setup rewards being nimble rather than positioned: two binary catalysts land in the same session, and the pre-holiday tape means thin liquidity likely amplifies whichever way the moves go before the Friday closure and Monday re-open.

Bullish Factors

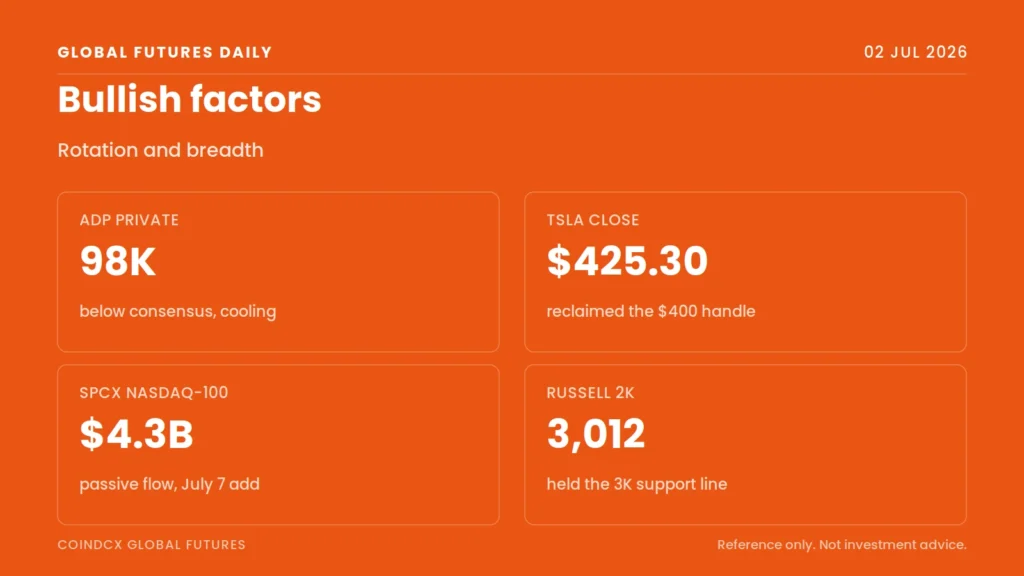

- ADP’s soft 98K private payrolls print argues for a cooler NFP that could revive the September rate cut trade and support rate-sensitive sectors.

- Tesla shares reclaimed the $400 handle on Monday and closed July 1 at $425.30, leaving room to run on any Q2 delivery beat above 410K.

- Communications services and financials led Wednesday’s tape as the market broadened away from Mag7, a healthier internal signal than a narrow tech-only rally.

- SpaceX – SPCX joins the Nasdaq-100 effective July 7, with JPMorgan estimating roughly $4.3B in passive inflows around the rebalance.

- Russell 2000 held the psychologically important 3,000 mark, closing at 3,012.59 with breadth positive despite the tech pullback.

- Cramer’s AI-supplier thesis – MU, INTC, MRVL, AMD, SNDK is getting fresh attention as Wall Street rewards chip and infrastructure names over the hyperscalers funding them.

Bearish Factors

- The two-day tech relief rally unraveled on the first session of Q3, with Nasdaq off 0.66 percent and semiconductor names leading the fade.

- Any NFP print above 130K with wages hot puts the Fed’s pause-through-year-end narrative back in play and pressures long-duration tech.

- White House economic adviser Hassett previewed ‘another strong number’ on CNBC, signaling upside risk to the headline print.

- Tesla Q1 left about 50K units of inventory overhang. A Q2 delivery print below 390K would confirm demand deterioration rather than tax-credit noise.

- Fed Chair Warsh’s Sintra remarks offered no dovish shift, leaving the market pricing rate cuts later than most sell-side strategists want.

- Thin pre-holiday liquidity means whichever direction NFP surprises, the market response is likely to overshoot before Monday’s re-open.

Asian Markets This Morning

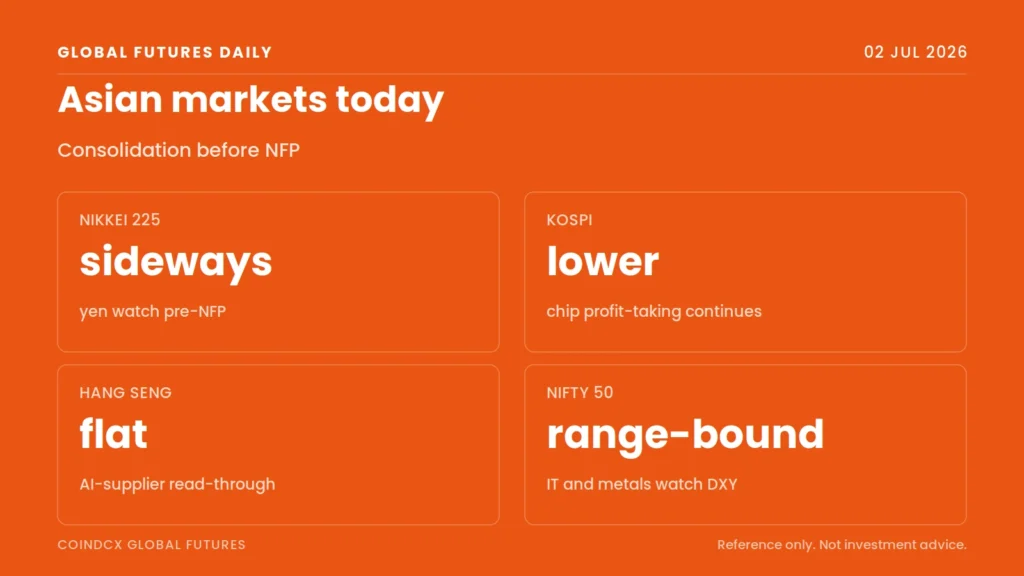

- Nikkei 225 trading sideways as the yen stays under pressure and traders await NFP for direction on USD/JPY carry positioning.

- Kospi lower on continued profit-taking in semis after the H1 chip rout, with the SK Hynix ADR SKHY roadshow prep in focus.

- Hang Seng consolidating with a mainland-tech watch for AI-supplier read-through from Cramer’s thesis.

- Nifty 50 range-bound through Wednesday, with IT and metal names watching NFP for dollar-index direction.

What Moved Wall Street Yesterday

Wednesday opened Q3 with an intraday high before drifting into the close. The Dow shed 14 points to finish at 52,305.24, the S&P 500 fell 0.22 percent, and the Nasdaq gave back 0.66 percent as the two-day tech relief rally that closed Q2 came undone. The Russell 2000 also faded from an intraday high but held 3,000 with a close at 3,012.59. Communications services and financials were the two lifting sectors, an unusual pairing that signals broadening rather than pure risk-on. ADP private payrolls at 98K printed below consensus, the softest reading in three months and a real-time argument that the labor market is cooling. Fed Chair Kevin Warsh spoke on a panel at the ECB Sintra Forum alongside Lagarde, Bailey, and Macklem, but stayed away from forward guidance on the US rate path. Kroger announced a $1.65B acquisition of Giant Eagle. SpaceX – SPCX traded lower after Monday’s 7.2 percent surge on the confirmed Nasdaq-100 inclusion, with sell-side flagging roughly $4.3B in expected passive rebalance inflows into the July 7 add.

Assets in Focus

- TSLA Q2 deliveries drop today. Bloomberg consensus 397K, Tesla IR consensus 406,024 – median 408,609. Closed July 1 at $425.30. Beat above 410K signals demand recovery, miss below 390K confirms Q1 inventory overhang worsening. Q2 energy storage consensus 13.8 GWh vs. 8.8 GWh in Q1.

- SPCX Nasdaq-100 inclusion effective July 7. Traded -1.74 percent premarket Wednesday after Monday’s +7.2 percent on the confirmed inclusion. JPMorgan sees roughly $4.3B in passive inflows around rebalance.

- NVDA / AMD / MU Semiconductor names lagged in the Q3 opening session as the tech relief rally unwound. Cramer’s AI-supplier thesis drives near-term rotation setup. MU still near ATH after last week’s Q3 print.

- MAGS Roundhill Mag Seven ETF traded +0.16 percent premarket Wednesday, but the Mag7 lost roughly $2.3T in market value in June on AI-monetization skepticism. Watching for a post-NFP directional break.

- KR Announced $1.65B acquisition of Giant Eagle. Shares fell 2.8 percent premarket on integration and antitrust overhang risk.

- GLD / DXY Both react to NFP first-order. A hot print strengthens the dollar and pressures gold. A soft print pulls yields lower and gives gold room to recover from the June flush.

Index Levels to Watch

- Russell 2000: 3,000 support defended Wednesday, 3,050 upside pivot for breakout continuation.

- S&P 500: 7,400 support at Wednesday’s intraday low zone, 7,470 resistance at Tuesday’s H1 close level.

- Nasdaq Composite: 26,000 psychological support, 26,300 resistance from Tuesday’s H1 close highs.

- Dow: 52,000 support, 52,500 resistance zone.

Disclaimer

This article is for informational purposes only and is not investment advice. Trading in US Stock Futures, crypto assets, and other instruments carries risk including the potential loss of principal. CoinDCX does not provide trade recommendations and the price levels referenced are context points, not entry or exit signals. Crypto products and Virtual Digital Assets (VDA) are unregulated and can be highly risky. There may be no regulatory recourse for any loss from such transactions. For any queries, visit support.coindcx.com

Frequently Asked Questions

Q1. Why is NFP dropping on Thursday instead of Friday?

US equity and bond markets close Friday, July 3 for Independence Day observance because July 4 falls on a Saturday. The BLS moved the June Employment Situation release forward one session to Thursday, July 2 at 8:30 AM ET, which is 6:00 PM IST.

Q2. What is Wall Street expecting from Tesla's Q2 deliveries?

Tesla's own investor-relations consensus is 406,024 vehicles with a median of 408,609. Bloomberg consensus is roughly 397,000. A beat above 410K is read as a demand-recovery signal. A miss below 390K signals the Q1 inventory overhang is worsening rather than resolving.

Q3. What did Fed Chair Warsh say at the ECB Sintra Forum?

Warsh spoke on a global central bankers panel alongside Lagarde, Bailey, and Macklem, but stayed away from forward guidance on the US rate path. The market read his tone as neutral, leaving rate-cut pricing broadly unchanged.

Q4. Which sectors led the tape on July 1?

Communications services and financials were the two sectors doing the lifting, in contrast to semiconductors and Mag7 tech which faded from Tuesday's Q2 close highs. That pairing tends to signal broadening participation rather than a narrow risk-on move.

Q5. Where can I trade US stock perpetuals from India?

CoinDCX Global Futures offers perpetual contracts on major US-listed names including TSLA, NVDA, AMD, MU, SPCX, MSFT, AMZN, META, GOOGL, AAPL, and NFLX, with rupee funding and up to 5x leverage.

{kind=link}

{kind=link}