Kospi crashed 7% overnight as SK Hynix and Samsung sold off, Brent jumped 3.5% on Hormuz strikes, and US futures slipped into CPI Week and Warsh testimony.

TLDR

- Kospi crashed as much as 7% overnight to its lowest close since May 4, as SK Hynix and Samsung led profit-taking that dragged the Nikkei down about 1.5% alongside it.

- Brent crude jumped over 3.5% after weekend strikes escalated across the Strait of Hormuz, pushing US futures lower and reviving Fed rate-hike bets.

- SK Hynix begins regular-way trading on the Nasdaq today under the permanent ticker SKHY after Friday’s $168.01 close, up 13% from the $149 IPO price.

- US markets have no data or earnings today, but June CPI and Chair Warsh’s House testimony both land Tuesday, with JPMorgan and four other big banks reporting the same morning.

- S&P 500 futures were down about 0.34%, Nasdaq-100 futures led the drop at 0.54%, and Dow futures fell around 0.27% in early trade.

Market Regime

Wall Street enters this week riding a two-part tension. On one side, the S&P 500 sits at 7,575, the Nasdaq at 26,281, and Meta just posted its best week since early 2024 as the AI trade broadened beyond the pure semis. On the other, weekend strikes across the Strait of Hormuz have re-opened the energy channel that markets thought was closed after the June ceasefire, and Asia has already repriced that risk hard overnight.

The rest of the week is set up to force a choice. Tuesday brings June CPI at 8:30 AM ET and Chair Warsh’s first congressional testimony 90 minutes later, on the same morning JPMorgan, Bank of America, Goldman, Wells Fargo, and Citi report. A soft headline print driven by June’s since-reversed oil dip could get a jump, but a firm core at 2.9% keeps the September hike bet alive, and Warsh’s hawkish tilt from the June dot plot is still fresh. Today’s session is likely the calmest one this week.

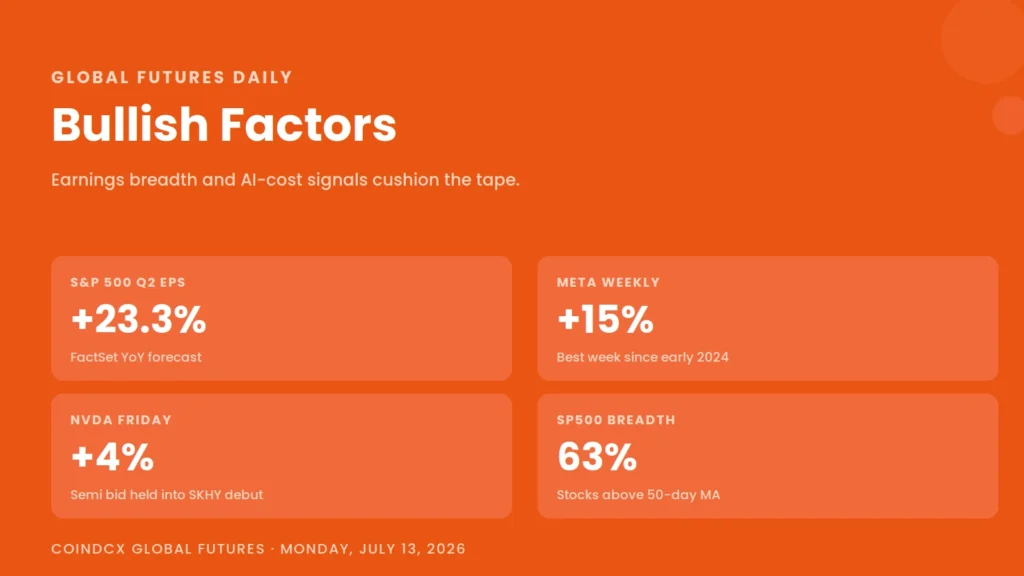

Bullish Factors

- Meta’s 15% weekly gain on improving AI-cost signals broadened the tech leadership away from a pure semi trade, and Nvidia’s 4% Friday close showed the flagship still bid into the memory rotation.

- Q2 earnings kick off Tuesday with FactSet forecasting 23.3% YoY S&P 500 earnings growth, the highest since 2021 and a genuine fundamental support if the big banks confirm consumer resilience.

- The SKHY debut clears an AI-memory overhang that was holding back the semi trade, and Bernstein and TrendForce see Samsung’s HBM share rising toward 37% into year-end, meaning both Korean names have room to work.

- Market breadth has healed: about 63% of S&P 500 stocks now trade above their 50-day moving averages, up from 50% a month ago, with small caps and financials joining the tape.

- A soft June CPI headline print is the base case for Tuesday, and even a rate-hike-hedged desk sees gasoline-driven disinflation buying the Fed some optionality before the July 29 FOMC.

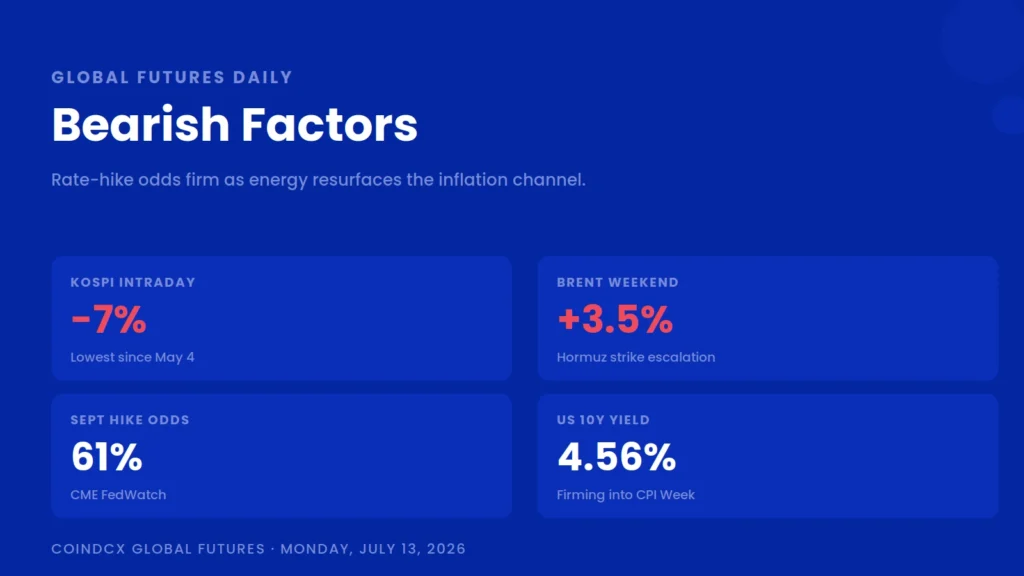

Bearish Factors

- The Kospi’s 7% intraday drop is a live warning that AI-memory positioning is crowded, and any spillover into US semis on the SKHY debut day could hit NVDA, MU, and the broader chip complex.

- Brent’s 3.5% jump on Hormuz escalation reintroduces exactly the energy-price shock that drove May CPI to 4.2% headline, and it lands the same week traders were expecting a soft June disinflation print.

- The Fed’s June dot plot already pushed the 2026 median fed funds path up to 3.8% from 3.4%, and futures now price roughly 61% odds of a September hike, which puts every basis point of core CPI on Tuesday under a microscope.

- The 10-year yield at 4.56% and a firming dollar into CPI Week compress equity multiples right as the Nasdaq sits near record highs, and any hawkish Warsh line Tuesday could steepen that squeeze.

- One-year-ahead consumer inflation expectations rose to 3.7% in the June NY Fed survey, the highest since September 2023, keeping the sticky-inflation narrative alive underneath the headline print.

Asian Markets This Morning

Asia bore the brunt of the weekend risk-off. South Korea’s Kospi plunged as much as 7% intraday to its lowest level since May 4, with SK Hynix and Samsung Electronics leading the profit-taking after Friday’s SKHYV listing pop. Japan’s Nikkei fell around 1.5% as a chip-stock selloff compounded oil-driven cost concerns just as earnings season began. India’s Sensex opened more than 600 points lower before clawing back most of the gap, trading around 77,320 by mid-session, and the Nifty 50 dipped under 24,200 before recovering. Gold slid over 1% as the dollar firmed on revived rate-hike bets.

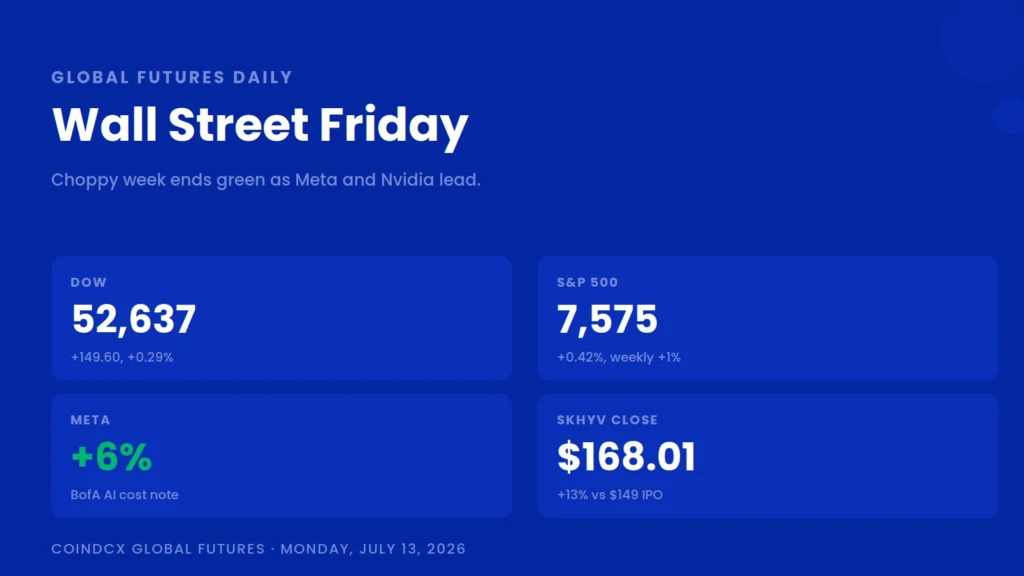

What Moved Wall Street Last Session

Friday closed a choppy week on the positive side. The Dow added 149.60 points, or 0.29%, to 52,637.01. The S&P 500 rose 0.42% to 7,575.39, and the Nasdaq Composite added 0.29% to 26,281.61. The week finished with the S&P 500 and Nasdaq both up about 1%, while the Dow slipped 0.5%.

Meta jumped about 6% on Friday to cap a nearly 15% weekly run, its best since early 2024, after Bank of America maintained its buy rating and pointed to an internal memo suggesting improving AI cost structure. Nvidia rose around 4% as chip demand cues from Applied Materials leadership supported the sector. SK Hynix’s ADRs opened at $170 in their Nasdaq debut and closed at $168.01, up 13% from the $149 IPO price, on demand that ran roughly seven times the available supply. Delta Air Lines beat on Q2 and reaffirmed guidance with a 15% dividend hike. Intel shed 2.4% and Broadcom lost 0.3% into the SKHY overhang.

Assets in Focus

SKHY (SK Hynix)

- Friday close: $168.01, up 13% from IPO

- Today: regular-way trading begins under the permanent SKHY ticker; SKUU and SKDD leveraged ETFs expected to list; options list Tuesday.

- Q2 earnings land July 29, giving markets 16 trading days to price the 13-year Korea Discount unwind versus AI-memory profit-taking.

NVDA (Nvidia)

- Friday close: up about 4% into the SKHY debut, extending Thursday’s memory-linked rally.

- Watch: spillover from the Kospi’s overnight 7% drop, where SK Hynix supplies more than half of the HBM inside NVDA’s AI accelerators.

META (Meta Platforms)

- Weekly: up nearly 15%, the best week since early 2024.

- Catalyst: BofA note pointing to improving AI cost structure; SemiAnalysis follow-through on Meta’s compute economics.

AAPL, GOOGL, AMZN, MSFT

- Big-cap tech into CPI Week: AAPL and AMZN print July 30, GOOGL July 28, and MSFT is expected the same window on July 29.

- The rate path priced Tuesday morning will set the multiple these names carry into their prints.

TSLA (Tesla)

- Q2 earnings confirmed for AMC July 22.

- Setup: the July 3 delivery-beat sell-the-news reaction leaves a wide error band around the print.

NFLX (Netflix)

- Q2 earnings confirmed for AMC Thursday, July 16, alongside TSM.

- Focus: ad-tier ARM and subscriber trajectory after the last quarter’s mixed guide.

XLE (Energy Sector)

- Setup: Brent’s 3.5% weekend jump on Hormuz escalation puts the energy tape back in the driver’s seat, reversing the June ceasefire disinflation trade.

NSDQ100 (Nasdaq 100)

- Level context: index near 29,824 heading into the week; futures down about 0.54% early Monday on the Kospi rout and Hormuz spike.

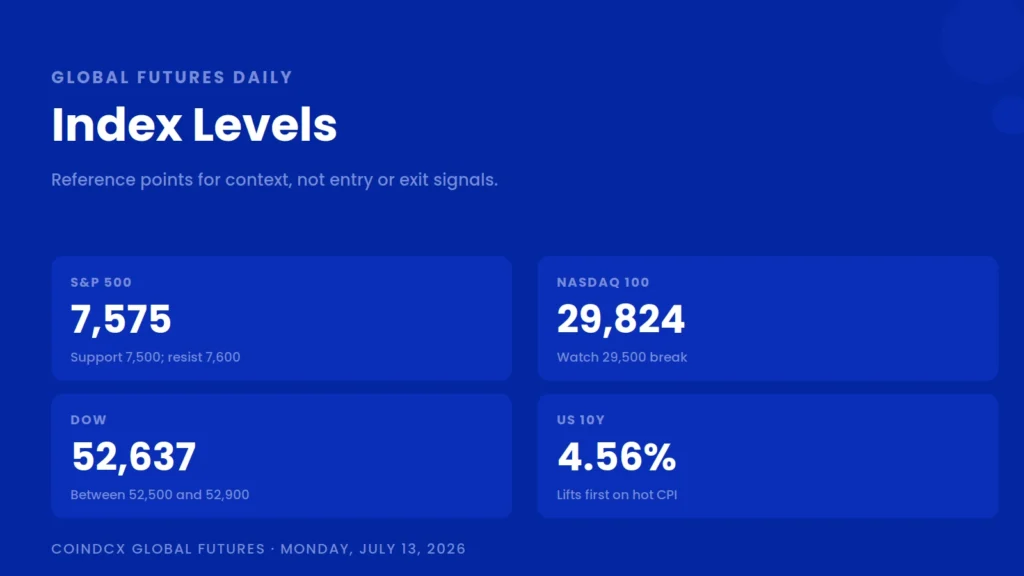

Index Levels to Watch

Brent Crude: up over 3.5% on the weekend Hormuz strikes; the direction of oil this session is the single biggest read on how sticky the CPI narrative gets.

S&P 500: Friday close 7,575.39. Round-number resistance at 7,600; short-term support around 7,500 into the CPI print.

Nasdaq Composite: Friday close 26,281.61. Nasdaq 100 near 29,824; a break below 29,500 would reset the tone into Warsh’s testimony.

Dow Jones: Friday close 52,637.01, after last week’s intraday all-time high near 52,742. Sits between 52,500 support and the 52,900 record close from July 3.

US 10-Year Yield: 4.56% into the week; a firmer CPI or hawkish Warsh line lifts yield first, equities second.

Disclaimer

This article is for educational and informational purposes only. It is not investment advice and should not be treated as a buy, sell, or hold recommendation for any security or financial product. Trading in futures and similar instruments involves significant risk including the potential loss of capital. Past performance is not indicative of future results.

Crypto products and NFTs are unregulated and can be highly risky. There may be no regulatory recourse for any loss from such transactions. For any queries, visit support.coindcx.com.

Frequently Asked Questions

Q1. Why did the Kospi crash 7% overnight when SK Hynix just had a strong US listing?

The two are connected. Friday's SKHYV Nasdaq debut priced at $149 and opened at $170 on demand roughly seven times oversubscribed, which pulled a lot of positioning into a single trade. That crowded setup collided with weekend strikes across the Strait of Hormuz, which lifted Brent over 3.5% and revived rate-hike expectations. When rate-hike odds firm up, high-multiple AI-memory names like SK Hynix and Samsung get sold first, and profit-taking from the ADR listing accelerated the move.

Q2. What time does SKHY start regular-way trading on Monday, July 13?

SK Hynix's American Depositary Receipts move from the temporary SKHYV ticker to the permanent SKHY ticker at the US open on Monday, July 13, 2026. Settlement occurs Tuesday, July 14, the same day options are expected to begin listing.

Q3. Why does the June CPI print on July 14 matter so much?

It is the last major inflation reading before the July 29 FOMC decision. Markets currently price roughly 61% odds of at least one Fed rate hike by year-end, and the Fed's June dot plot lifted the 2026 median funds rate to 3.8% from 3.4%. A hotter-than-expected core CPI reading Tuesday would harden that hike bet, while a soft print could unwind some of last week's hawkish repricing across yields, the dollar, and equities.

Q4. What is Fed Chair Warsh testifying about on Tuesday?

Kevin Warsh delivers his first semiannual monetary policy testimony to Congress on Tuesday at 10:00 AM ET, 90 minutes after the June CPI release. He is expected to speak on the Fed's policy stance, communication approach, the AI-driven productivity backdrop, and the five internal task forces he recently formed to review the central bank's framework. A hawkish tone would firm the dollar and pressure equities.

Q5. Are US markets closed today?

No. US equity markets are open for regular trading on Monday, July 13, 2026. There is no US economic data release scheduled for today and no S&P 500 earnings on the calendar. The heavy calendar begins Tuesday with CPI, Warsh, and the big-bank prints.

{kind=link}

{kind=link}